RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 1 |

RETHINK

DATA

Put More of Your Business Data to Work—

From Edge to Cloud

WITH RESEARCH AND ANALYSIS BY IDC

A SEAGATE TECHNOLOGY REPORT

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 2 |

About the Report ............................................................................ 03

Summary of Findings ...................................................................... 04

Survey Highlights ........................................................................... 05

Section I: Global Findings

Chapter 1: The Growth and Sprawl of Data ..................................... 07

Chapter 2: A Treasure Trove of Value ............................................... 13

Chapter 3: The Multicloud ............................................................... 19

Chapter 4: Data Management Challenges and

the Multicloud Ecosystem .............................................. 24

Chapter 5: DataOps: The Missing Link of Data Management ........... 29

Chapter 6: Better Business Outcomes ............................................ 33

Chapter 7: Data Security and Data Management ............................. 36

Section II: Regional Findings

Chapter 1: Asia Pacic and Japan ..................................................... 40

Chapter 2: China ............................................................................... 44

Chapter 3: Europe ............................................................................ 48

Chapter 4: North America ................................................................. 52

Table of Contents

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 3 |

About the Report

This Seagate Technology report

draws on a global survey sponsored

by Seagate and conducted by the

independent research rm IDC, which

took place in December 2019 and

January 2020. Seagate authored the

following report to share its forecasts

and opinions, based on the survey

ndings, along with analysis from

IDC. Any content, data, analysis, or

views not attributed to IDC or IDC

analysts are those of Seagate. The

quantitative web survey queried 1500

respondents globally (375 in North

America, 475 in Europe, 500 in APJ,

and 150 in China) from mid-sized

businesses to larger enterprises

in Canada, United States, United

Kingdom, France, Germany, Russia,

Australia, Japan, India, South Korea,

Taiwan, and China. The survey

participants’ professional titles

include CIO, CTO, IT VP, director,

executive, COO/LOB, storage

architect, and solution architect.

Seagate Technology has been a global leader offering data storage and

management solutions for over 40 years. Seagate crafts the datasphere,

maximizing human potential by innovating world-class, precision-

engineered data storage and management solutions with a focus on

sustainable partnerships.

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 4 |

Summary of Findings

Today’s unprecedented growth

and sprawl of data result in a

complex movement of data within

an increasingly varied ecosystem

that includes multicloud and the

edge. The complexity of data’s

location compounds business

owners’ data management

challenges. Most data available

to businesses goes untapped.

The survey zeroed in on a solution

to today’s data management

dilemmas: DataOps—a discipline of

connecting data creators with data

consumers. Business leaders who

implement DataOps can count on

better business outcomes.

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 5 |

Survey Highlights

• Over the next two years, enterprise

data is projected to increase at a

42.2% annual growth rate.

• Only 32% of data available to

enterprises is put to work. The

remaining 68% goes unleveraged.

• On average, organizations now

periodically transfer about 36%

of data from edge to core. Within

only two years, this number will

grow to 57%. The volume of data

immediately transferred from

edge to core will double, from 8%

to 16%. This means enterprises

will have to manage a lot more

data in motion.

• Managing data in the multicloud

ecosystem is a top data

management challenge expected

over the next two years—with

managing data in hybrid cloud a

close second.

• The top ve barriers to putting data

to work are: 1) making collected data

usable, 2) managing the storage

of collected data, 3) ensuring that

needed data is collected, 4) ensuring

the security of collected data, and 5)

making the different silos of collected

data available.

• The solution to a great deal of

data management challenges

is DataOps—the discipline

connecting data creators with

data consumers. Only an average

of 10% of organizations report

having implemented DataOps fully

across the enterprise. A majority of

respondents say that DataOps is

“very” or “extremely” important.

• Along with other data

management solutions, DataOps

leads to measurably better

business outcomes: boosted

customer loyalty, revenue, prot,

and a host of other benets.

• Improving data security is the

most important factor driving the

changes to how organizations

manage central storage needs.

• Two thirds of survey respondents

report insufcient data security,

making data security an essential

element of any discussion of

efcient data management.

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 6 |

Global

Findings

SECTION ONE

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 7 |

CHAPTER ONE

The planet’s population is at 7.8

billion and it keeps growing. More

and more people work from home.

Technologies like the Internet of

Things (IoT), the growth of edge

computing, edge data centers,

and articial intelligence (AI)

proliferate. Demand for consumer

endpoint devices is growing.

All these factors result in the

proliferation of enterprise data.

In order to smartly manage the ever-

accelerating amount of information,

business owners need to understand

how and where data is gaining in

volume. Two concepts help illustrate

this trend: growth and sprawl.

Data growth refers to the

percentage by which the

datasphere increases over time.

The datasphere is humanity’s ever-

expanding dimension of living data

that reects and amplies life in

innite ways.

Data sprawl describes the spread

of this growing data through

various congurations—from

endpoints through edge to cloud.

Data is who we are, who we have

been, and who we are becoming.

The Growth and the

Sprawl of Data

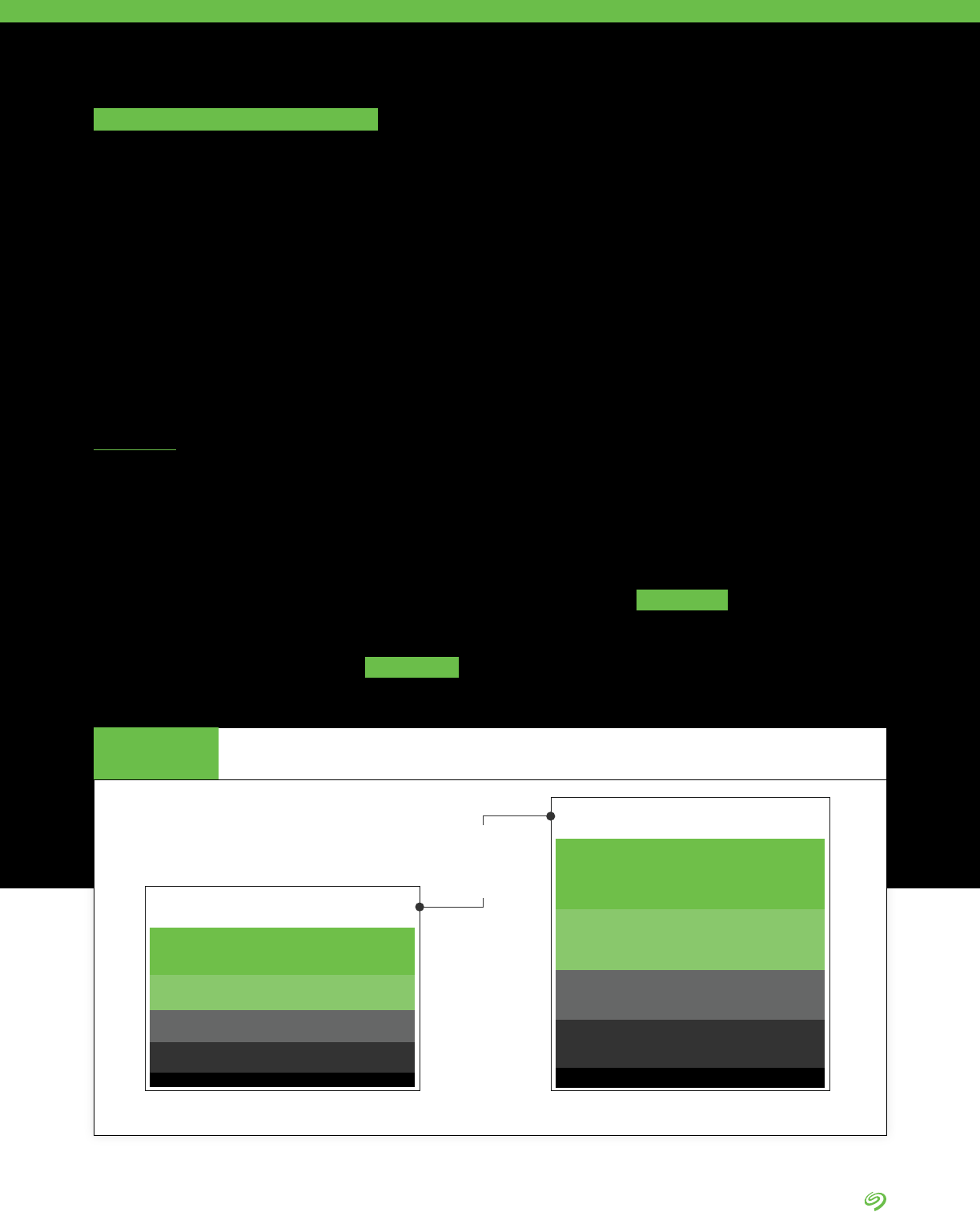

2020: Total Enterprise Data

Volume of 1PB

160TB in other locations

390TB in edge & remote locations

407TB in 3rd-party data centers

498TB in cloud repositories

(public, private, industry)

570TB in internally managed

data centers

89TB in other locations

193TB in edge & remote locations

201TB in third-party data centers

221TB in cloud repositories

(public, private, industry)

297TB in internally managed

data centers

2022: Total Enterprise Data Volume

of Approx. 2.02PB

+42.2%

avg. annual growth

over 2 years

Expected Annual Data Growth Rate

FIGURE 1

SEAGATE POV

Source: The Seagate Rethink Data Survey

1

, IDC, 2020

1 The Seagate Rethink Data Survey by IDC is IDC’s name for the survey whose ndings are discussed in this report.

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 8 |

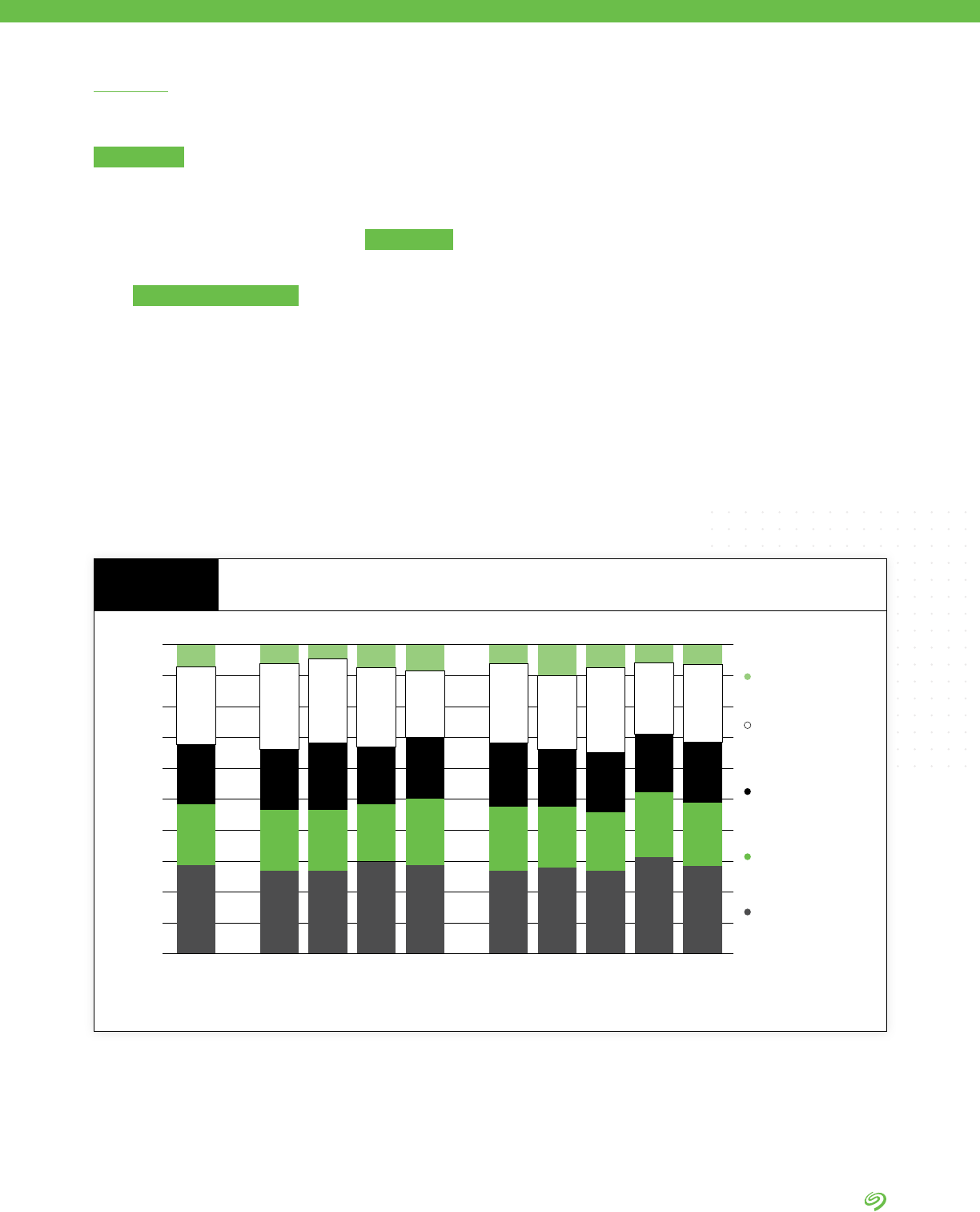

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Total NA China Europe APJ TelcoTrans/EV Media Mfg Other

Internally managed

enterprise data

centers

Third-party

managed enterprise

data centers

Edge data centers

or remote locations

where data is

centrally stored

Cloud repositories

(public, private,

industry)

Other locations

Data growth has been and will

continue to be unprecedented in

volume. The survey conducted

shows that in just two years, from

the beginning of 2020 through the

beginning of 2022, enterprises will

see a 42.2% annual increase in the

volume of generated data. In order

to project the volume of enterprise

data, IDC uses enterprise storage

capacity as a proxy (Figure 1).

The survey data indicates that three

factors are the most important

catalysts for the growth of stored data:

1. Increasing use of analytics.

2. The proliferation of IoT devices.

3. Cloud migration initiatives.

Data sprawl reects how business

data is scattered.

Enterprise data doesn’t reside in one

location, which adds complexity to

data management.

Survey respondents indicate

that approximately 30% of

stored data is found in internal

data centers, 20% in third-party

data centers, 19% in edge data

center or remote locations, 22%

in cloud repositories, and 9% in

other locations. This distribution

won’t change signicantly over

the next two years, indicating that

enterprise storage environments

will remain dispersed and complex

for the foreseeable future.

Enterprises will have an ever-

increasing need to manage this

scattered data wherever it exists.

Survey Findings

Where Data Will Be Stored in 2 Years (Average)

FIGURE 2

DATA BY IDC

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 9 |

Innovation is not driven by trends, but by the need to create more

value under constraints—and there are constraints everywhere.

Access to the full value of data is one of them.

Take a look at our data-driven world. Data is growing, and the

rate of growth is accelerating. The sum of data generated by 2025

is set to accelerate exponentially to 175 zettabytes. More data is

created per hour now than in an entire year just two decades ago.

Data is human potential. The sharpest minds attempt to harness

the power of data.

The constraints on capturing the full potential of data are both

systemic and operational. At zettabyte scale, there needs to be

a simple, secure, and economic way to capture, store, and activate

data. People who use the data do not want to worry about this.

How can we solve this data management puzzle at scale and

enable other innovations that change the way we live, work,

commute, and take care of our planet?

If we address the opportunities while navigating these constraints

and enable the most value, then does it matter whether the

innovation used the latest trend or not? Trends may capture our

minds, but if the initial excitement does not translate into value for

companies and for humanity, innovation doesn’t take hold.

When we solve problems at scale, we need to bring multiple

worlds together, and invite their synergy.

DAVE MOSLEY

CEO OF SEAGATE TECHNOLOGY

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 10 |

Delving Deeper

Additional research done by IDC

as part of the Global DataSphere

1

sheds light on why enterprises will

see so much data growth.

• The amount of new data

created each year is growing at

a compound annual growth rate

of about 26% between 2015

and 2025.

• The number will be up to 175.8ZB

of new data created in 2025

(compared to 18.2ZB in 2015).

• Enterprise data stored in 2025

will amount to 9ZB—while in

2015 was 0.8ZB.

• The Rethink Data survey backs

up this trend: respondents

consistently indicate that for

their organization, enterprise

data capture and storage

are expanding. It indicates

that the increasing use of

analytics, increasing use of IoT

devices, and cloud migration

initiatives are the top three most

important factors impacting the

growth of stored data.

• Leveraging the Global

StorageSphere

2

and Global

DataSphere studies, we can

better understand data sprawl.

• The Global DataSphere indicates

that 65% of data created in

2015 was at endpoints, and

35% in the core and edge.

• By 2025, the 44% of data

created in the core and edge will

be driven by analytics, articial

intelligence, and deep learning,

and by an increasing number of

IoT devices feeding data to the

enterprise edge.

• Data is shifting to both the core

and the edge: By 2025 nearly

80% of the world’s data will be

stored in the core and edge, up

from 35% in 2015.

• By 2025, IDC predicts 12.6ZB of

installed capacity—HDD, ash,

tape, optical—will be managed

by enterprises. Cloud service

providers will manage 51% of

this capacity.

Endpoint-Create

Endpoint-Store

Edge-Create

Edge-Store

Core-Create

Core-Store

80%

70%

60%

50%

40%

30%

20%

10%

0%

20112010 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Where Data Is Created and Stored

FIGURE 3

DATA BY IDC

1 Data Age 2025, sponsored by Seagate, with data from Global DataSphere, IDC, May 2020

2 The Global StorageSphere, IDC, 2020

Source: Data Age 2025, sponsored by Seagate, with data from IDC Global DataSphere and StorageSphere, May 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 11 |

The edge can be found anywhere

and everywhere, in a wide range

of locales, including:

• Floors of manufacturing plants

• Roofs of buildings

• Cell phone towers in the eld

• Barns on farms

• Autonomous vehicles

• Platforms at oil and gas elds

The edge is a location, not a

thing. It is the outer boundary of

the network—sometimes found

hundreds or thousands of miles

from the nearest enterprise or

cloud data center, and as close to

the data source as possible. The

edge is where real-time decision-

making takes place.

What Is the Edge?

More and more data needs

analysis and action at the edge.

A unique mix of technology and

economics will make it practical

to assemble, store, and process

more data at the edge.

The shift of data’s center of

gravity to the edge is driven by

four technologies:

1. AI has become cost-effective

and practical.

2. Billions of IoT devices are being

deployed.

3. Wireless operators are upgrading

their networks to the fth

generation of cellular mobile

communications (5G).

4. Innovations in edge data centers

are solving for the complexities

of distributed facilities and unit

cost economics.

In addition to these technologies,

key factors drive demand for

edge computing: latency; high

data volume accompanied by

insufcient bandwidth; cost; and

data sovereignty and compliance.

As massive amounts of data are

created outside the traditional data

center, the cloud will extend to

the edge. It won’t be cloud versus

edge; it will be cloud with edge.

Giving Data an Edge

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 12 |

The amount of data stored at the

edge is increasing at a faster rate

than data stored in the core.

This survey found that, on average,

organizations periodically transfer

about 36% of data from the edge to

core. Within only two years this

percentage will grow to 57%.

The volume of data immediately

transferred from edge to core will

grow from 8% to 16% as well. To

accommodate this increase, data

management plans must enable a

much more signicant movement of

data—from endpoints, through edge,

to public, private, or industry clouds.

What does this mean for

enterprises?

It means a greater extent of data

sprawl, which enterprises are

increasingly tasked to manage.

Data sprawl leads to siloed data,

which cannot be accessed by all

who need it. Without automated

methods, managing data sprawl

requires signicant human labor and

redundant tool purchases.

An increasing amount of storage

will be expected to be compute-

conversant—if not, eventually,

offering compute functions.

The edge is expected to store

critical data and insight that

fuels latency-sensitive requests

from endpoint transactions and

services. At the same time, the

edge will make possible distributed

computing to perform analysis of

streaming data.

Streamed data is likely to be cached

in storage media until the servers

complete analytics.

As such, the line between

storage and caching of data at

the edge may become blurred,

especially given the expectation that

data will be stored for only a short

period of time until it is analyzed or

processed before moving relevant

data to the core.

In Focus: Data at the Edge

ANALYSIS BY IDC

Periodically

transferred to core

2020

Immediately

transferred to core

Mix of models

2022

Collected and

stored at edge

2022

2020

2022

2020

2022

2020

2022

2020

14%

8%

38%

15%

36%

57%

8%

16%

Approach to Collecting Data at the Edge

Now vs. Two Years From Now

FIGURE 4

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 13 |

CHAPTER TWO

Winning enterprises know that how

they treat their data can directly

translate into business growth.

To businesses entrusted with

data—for example, cloud

providers, smart devices

manufacturers, hospital networks,

streaming networks, grocery store

chains, just to name a few—data

means investment into collecting,

analyzing, and storing data in

various repositories.

The more they can leverage their

investment by putting that data

to use, the more value they will

derive from it.

The datasphere contains an ever-expanding

kaleidoscope of human endeavors: urgent life-

critical information, histories of knowledge,

operational instructions, manufacturing

processes, chronicles of emotion, etc.

Data is a treasure trove of value.

A Treasure Trove of Value

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 14 |

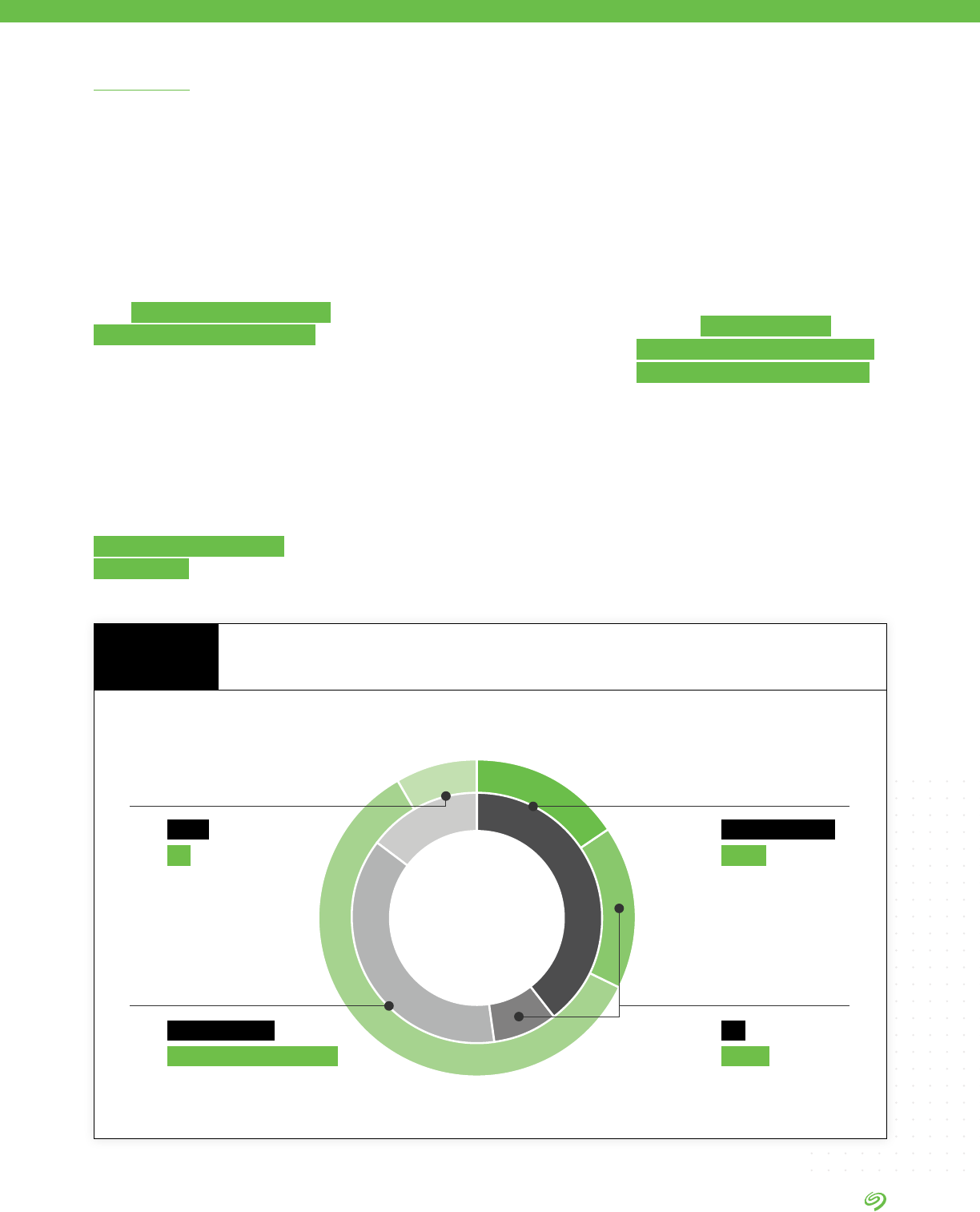

Missing Out on Data

The Rethink Data survey has found

that organizations report that much

of their business data is not put

to use, or activated. While the data

offers value, that value too often

goes uncaptured.

• Survey respondents estimated

their organizations collect only 56%

of the data potentially available

through its operations. This means

organizations are missing out on

almost half of data.

• Out of that 56%, only 57% of data

was used by the organization.

• 43% of the captured data went

largely unleveraged.

• This means that only 32% of the

data available to enterprises

was put to work. As much as

68% of data goes unleveraged.

of captured data

is exploited

57%

43%

of data goes

uncaptured

44%

of data is captured

through operations

56%

remains

largely unused

How Much Data Actually

Gets Put to Work?

FIGURE 5

DATA BY IDC

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 15 |

Overall, for many organizations,

data is an understated, intangible

asset that is not represented

on the balance sheet—even

though data is increasingly being

leveraged to drive new sources

of revenue and improve customer

experiences and operational

efciencies. Simply stated, data

can increase enterprise value even

without being formally represented

in nancial statements.

However, to realize the value of

data, it must be put to work. The

survey established that only 32%

of the data available to enterprises

was leveraged.

Putting data to work and unlocking

its value rst requires a method for

measuring the value of the data itself.

In a survey conducted for Seagate in

2018

1

, IDC found that the workforce

in only 25% of organizations

worldwide had systems and

processes for actively quantifying the

value of enterprise data, at least in

certain situations.

Opportunities abound for

organizations to better leverage

data for competitive advantage.

In the same survey, only 11% of

all organizations reported that

they considered themselves to be

industry leaders in the ability to

leverage the value of corporate data

compared to other organizations

in their industry. The percentage

was even lower for the healthcare

and transportation industry

verticals, where fewer than 10% of

organizations identied themselves

as industry leaders.

One thing is certain: Companies

want to have vibrant data lakes

where fresh data is taken in

and old, stale data is moved to

low-cost storage domains. No

company wants their data lake

to turn into a data swamp where

unleveraged yet potentially

useful data sits dormant on

storage media.

The value of data for any given

enterprise involves numerous

variables, including the industry

within which it is created, the

purpose it serves, and if and how it

is eventually monetized.

Take, for example, the types of

data created and managed by a

hospital: patient data, scheduling,

insurance and billing data, MRIs,

cancer treatments, operations and

nancial data, and advertising.

Regulations require that hospitals

keep data for many years after

the death of a patient (this is likely

dormant data that potentially can

be leveraged). The value of each

dataset will vary, especially data that

is highly secure due to privacy and

compliance requirements. In the

future, video sessions for remote

care, the surgeon’s actions during an

operation, or even robotic operation

procedures will be recorded and

saved for a variety of reasons—even

if only to serve for instructional or

legal purposes. Can one really place

a value on this data?

IDC has yet to fully quantify the

value of the global datasphere.

Nevertheless, making some general

assumptions about the value of a

byte created in a hospital with a staff

of 1000 to 2500 and revenues of

over $1B, IDC believes it is likely the

value of data created at that hospital

could be approaching several

hundred million dollars.

The Value of Data

ANALYSIS BY IDC

1 Worldwide DATCON and VoB surveys, IDC, September 2018

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 16 |

Every business is a data business. But enterprise data is of little

value if it is not used. To efciently and smartly make sense

of data, we need to see data lakes as reservoirs where many

vibrant rivers meet; the task is to comingle the incoming

data currents. There is a need to share data with other lakes,

in order to cross-reference and run analytics on disparate

streams of data.

Take autonomous cars. To begin with, there’s value in

analyzing data from one vehicle, and within one company.

Cross-analyzing that one vehicle’s data with vehicles from all

autonomous car companies adds another layer of insight. For

a richer picture, zoom out from there to integrating knowledge

derived from that one vehicle’s data with data that proceeds

from the billions of sensors that make up a smart city. The

fuller picture may be useful to the regional government and

city planners who implement better public safety standards

and trafc ows.

The more pieces you put together, the bigger a puzzle you can

solve. You can tackle a much higher-order problem if you share

data, cross-referencing various streams of information for analysis.

That’s why enabling the movement of data matters. Data needs

to move in order to allow for interconnectedness of data—and the

insights that result.

RAVI NAIK

SENIOR VICE PRESIDENT AND CIO

OF SEAGATE TECHNOLOGY

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 17 |

Organizations must be able to

capture the right data, identify it,

store it where it is needed, and

provide it to decision makers in a

usable way.

Activating data—putting it to

work—starts with data capture.

Given the exponential growth

of data due to growing IoT

applications, enterprises do not

currently capture all available

data. To do so would result in

an overworked IT infrastructure

and tremendous costs. Without a

solid data management solution,

companies need to leverage

data ingest software capabilities

to identify and classify data at

the beginning of data lifecycle.

With proper identication and

classication, automated policies

can keep data through its useful

period, and then delete or archive

it when it is no longer needed. This

data pruning lowers costs and

avoids clogging data management

efforts. However, as data

management solution technology

advances, companies can consider

capturing more data, which can be

utilized for improving their articial

intelligence or machine learning.

Data capture then feeds into

data analysis. Most often, it’s

done in data lakes where data

is assessed by specialized data

analysis software based on industry

or other criteria. Data curators

and scientists use these tools to

mine information from the data to

provide to decision makers. Data

ingest into a data lake eliminates

the silos that separate data and

allow connections to be made from

seemingly unrelated data elements.

This is what leads to competitive

advantage.

Storage is integral to an

organization’s data strategy as it is

an active contributor to the process

of sorting and analyzing information.

The need for accurate, real-time

reporting of stored data to improve

workows, security, and resource

management initiatives continues

to drive demand for advanced data

management and analytics solutions.

Putting Data to Work

“Whether structured,

semistructured,

or unstructured;

generated by humans

or by machines; or

stored in the data

center or the cloud,

data is the new

basis of competitive

advantage.”

PHIL GOODWIN

RESEARCH DIRECTOR, IDC

At the Edge

Edge devices pose a particular challenge for data capture. Often, only the edge application knows what data

needs to be captured and acted upon, and what data is transient and thus can be ignored. A lot of decision-

making has to happen close to where data is created. But the newer centralized data management ingest

applications can leverage articial intelligence (AI) and machine learning (ML) to make the determination. These

programs can often identify sensitive data (like personally identiable information, private health information, credit

card numbers, etc.) and automatically mask them from the view of unauthorized personnel. This reduces the

chance of a data breach or inadvertent data disclosure.

ANALYSIS BY IDC

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 18 |

Storage Innovation and the Value of Data

How and where data is stored

can greatly affect the value that

organizations can derive from it.

Here are areas in which storage

innovations bear directly on the

value of data.

1. Mass capacity is the enabler of

economies of scale. Analytics

improve as the data sets

that they access grow. Good

data management includes

ensuring that any new AI or ML

breakthroughs have access

to all of the data (as much as

physically possible). That is

why data storage companies

like Seagate focus on the

development of areal density

growth (so devices can store

more on a given unit).

The focus on areal density

innovation is based on data from

the world’s largest clouds.

Companies distribute data

roughly along the 90/10 rule:

90% of their data is stored on

hard drives and 10% on ash

memory devices (SSDs).

2. Another focus of storage

innovation has been delivering

higher bandwidth in order to

catalyze more robust movement

of data among storage,

networking, and compute

functions. This is important

for analytics. The backbone of

today’s analytics is the GPUs

(graphics processing units).

They require high bandwidth

ingest of information. To improve

bandwidth, for example,

organizations use composable

disaggregated architectures in

large-scale AI applications.

3. Security is another area of

innovation. There is continued

investment in device integrity

through open enclaves for

making rmware and compute

carry and house appropriate

protocols to digitally verify

devices. System solutions

benet from securities at the

component and device level.

Networking’s security benets

from the system’s security.

Finally, compute is made more

secure as a result of more

security networking.

4. In the longer term, data

movement architectures will

need to ensure that hardware

acceleration or hardware ofoad

through the storage systems

is done at appropriate points.

Specically, compression,

encryption, and deduplication

of data sets today get done

in compute. As a result, big

architectures are having to scale

because these tasks are done at

the higher level. This need not be

the case if innovation moves the

hardware acceleration and ofoad

to the storage or network layer.

5.

6.

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 19 |

CHAPTER THREE

Enterprises often struggle with

access to some of their data that

resides in the public cloud. They

also have a hard time with moving

data out of the cloud—not to

mention the fees that come with

the retrieval. This can stand in the

way of deriving optimum value from

data in the public cloud context—

because to be valuable, data has

to move. As a result, enterprises

increasingly mix up their storage

options, choosing to manage data

in the multicloud ecosystem.

Multicloud means the use of

more than one public cloud, which

is orchestrated through data

management. It may also include

a private cloud component. In

practice, multicloud can mean that

an enterprise houses some data in

public clouds and some in on-prem

private cloud.

Repatriating some data to private

cloud ensures a mesh of benets

from private cloud and from the

multicloud ecosystem.

1. Predictable economics at scale, which are under an enterprise’s control.

2. IP ownership, protection, and control of where that data physically

resides. This is useful, for example, in cases of data that needs a clear

audit trail or must comply with regulatory requirements.

3. Frequent access to large data sets. This is advantageous because

storage becomes very expensive when businesses need to read and

analyze the data frequently.

4. Compliance with regard to sensitive data sets. For example, life-

critical data that requires a certain provider’s and patient’s locality, as well

as compliance with laws and regulations such as HIPAA and GDPR.

The public cloud has catalyzed the growth of

countless companies. When enterprises reach

scale, however, they nd public cloud alone

too inexible.

The Multicloud

Private cloud offers the following advantages:

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 20 |

1. Fast growth and scale. In the multicloud, teams can build and deploy

an application or service in a common environment—plus benet from

the resulting revenue stream—without an investment in CapEx to do so

globally.

2. Access to a broad catalog of services that include applications,

compute, and monitoring resources. The multicloud features the ability

to turn on a high-performance compute that would be unaffordable

in most private clouds. GPUs can run between $500 thousand and

$5 million. Access to the public cloud means businesses can rent

them, solve a puzzle, and be done with them without leaving them to

sit idle. Access to public cloud compute means maximum compute

horsepower that enables an efciency growth and elimination of

stranded resources.

The public cloud benets that extend to the

multicloud ecosystem include:

Hybrid cloud seamlessly fuses

the resources of private and

public clouds to deliver an

integrated infrastructure as a

service. Hybridization ensures

communication between clouds

and interoperability, or the ability to

work across resource boundaries.

What does it look like? For

example, a company buys an OEM

enterprise service and puts it in a

colocation environment in a shared

building and connects to a cloud

service provider’s protocol on the

back end.

Hybrid cloud tends to be under one

software management portal, which

does the heavy lifting of connect;

the application knows how to talk to

the lead software layer.

In multicloud, the application,

which tends to be built as cloud-

native, knows how to use and run

the resources. Hybrid clouds often

have to gure out how to take

legacy systems and connect them

to the benets of public cloud.

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 21 |

50%

Public Cloud

51%

Enterprise Private Cloud

36%

Hosted Private Cloud

37%

Multicloud

37%

Hybrid Cloud

17%

Industry Cloud

1%

Other

IDC analysts describe the multicloud

as “an organizational strategy or

the architectural approach to the

design of a complex digital service

that involves consumption of cloud

services from more than one cloud

service provider.” These may be

directly competing cloud services,

such as public object storage from

more than one public cloud service

provider, or IaaS and SaaS from one

or more cloud service providers.

According to IDC, in both of these

contexts, multicloud encompasses

a much larger universe than

does hybrid cloud and is only

gated by the cost and complexity

associated with enabling consistent

management and governance of

many different cloud options.

Multicloud as Organizational Strategy

Which of these cloud types is used in the

organization’s IT infrastructure?

FIGURE 6

Managing Data in More Than One Cloud

Survey respondents indicate a

wide range of cloud deployments,

including adoption of multiple cloud

service providers:

• The study reveals an equal

adoption of both multicloud and

hybrid cloud deployments (37%

each).

• Hybrid cloud use is typically

application-driven. The use of more

than one cloud develops organically

over time, with different lines of

business purchasing different cloud

providers for specic tasks.

• Businesses using multicloud

report that they do not necessarily

have a cohesive integration plan

for the long term.

• Multicloud and hybrid cloud

environments solve a number

of different problems. They

can make access to data and

analysis easier, cut costs, offer

administrators better control, and

boost data security.

But multicloud and hybrid cloud

ecosystems also pose some

challenges when it comes to

data management.

DATA BY IDC

ANALYSIS BY IDC

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 22 |

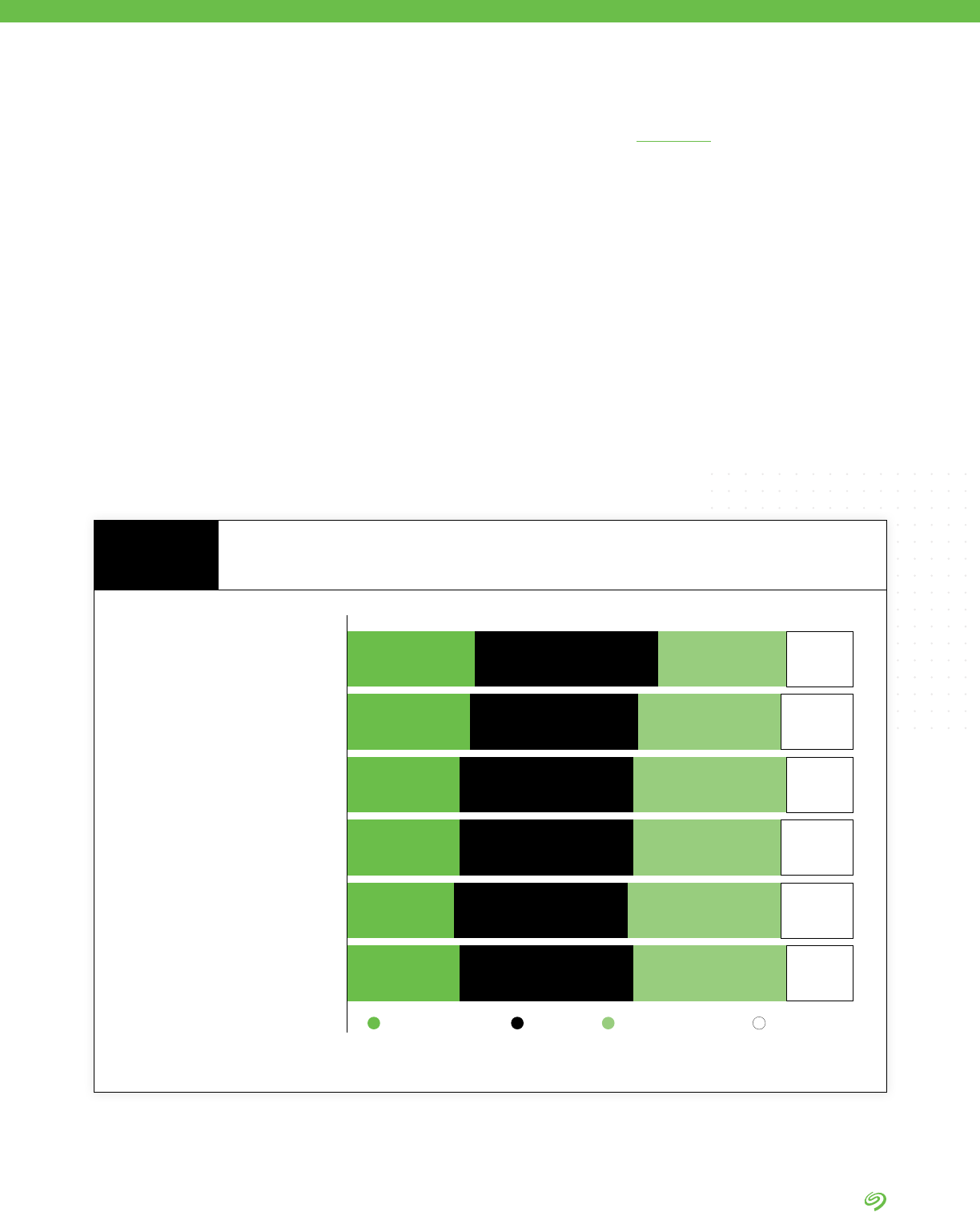

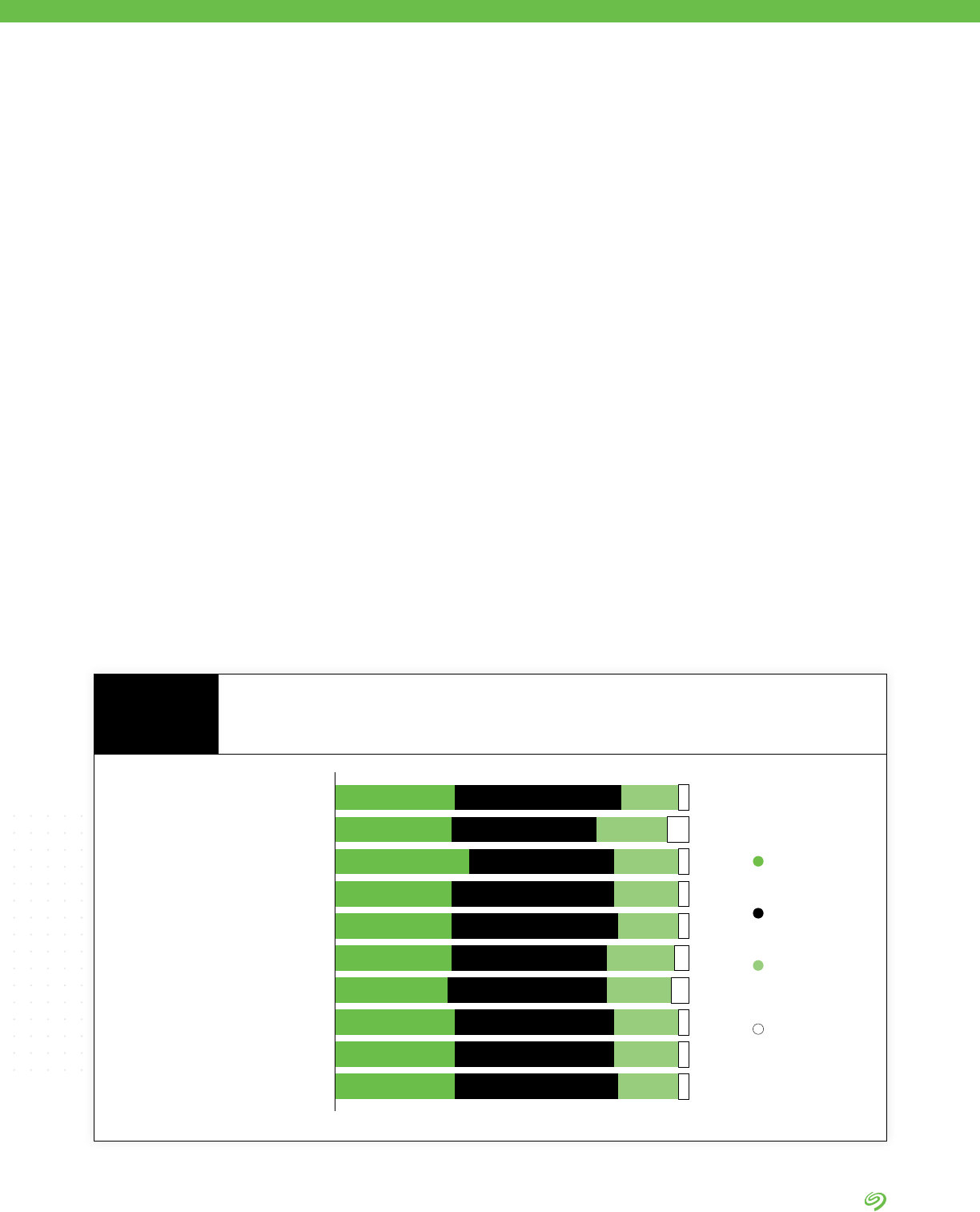

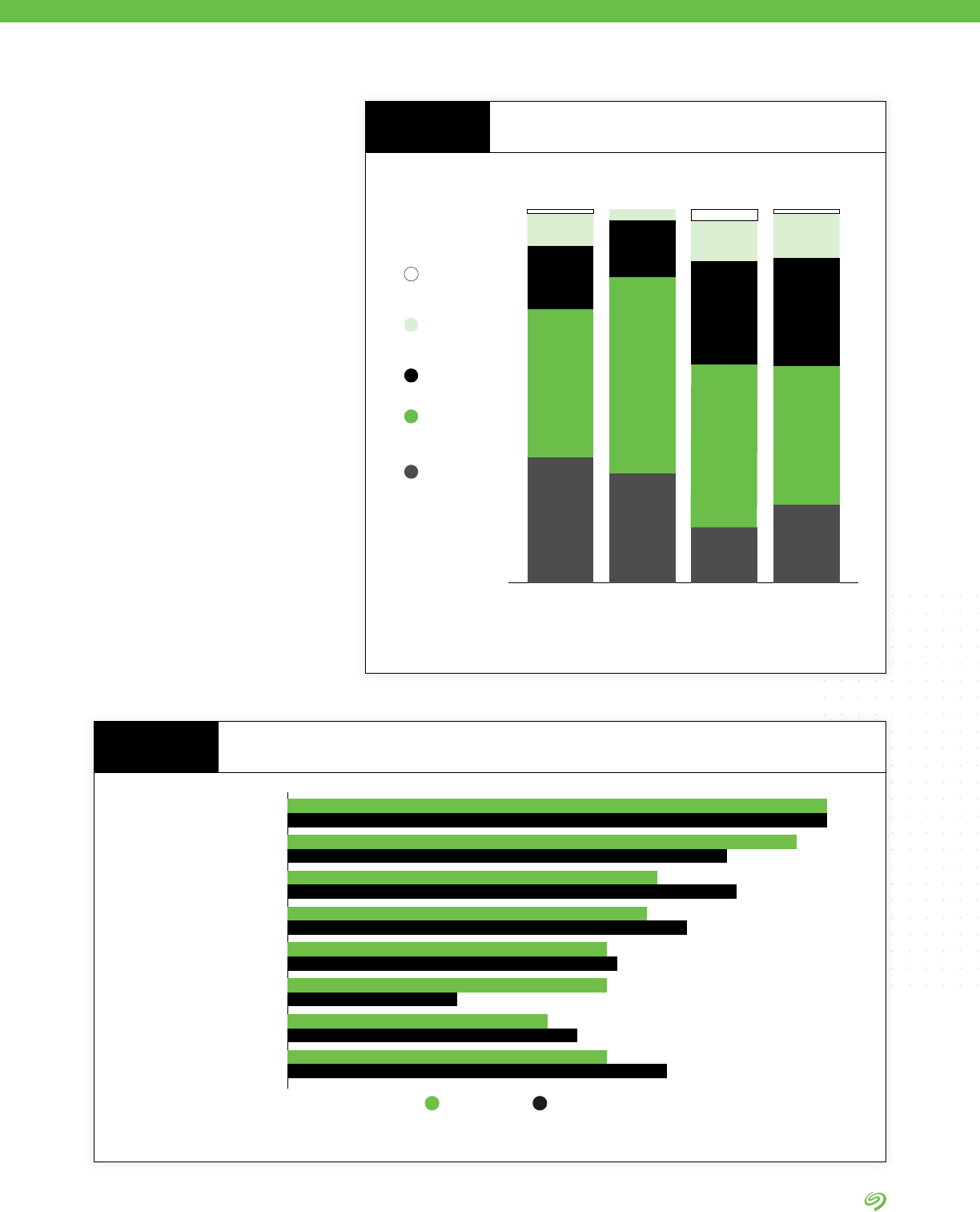

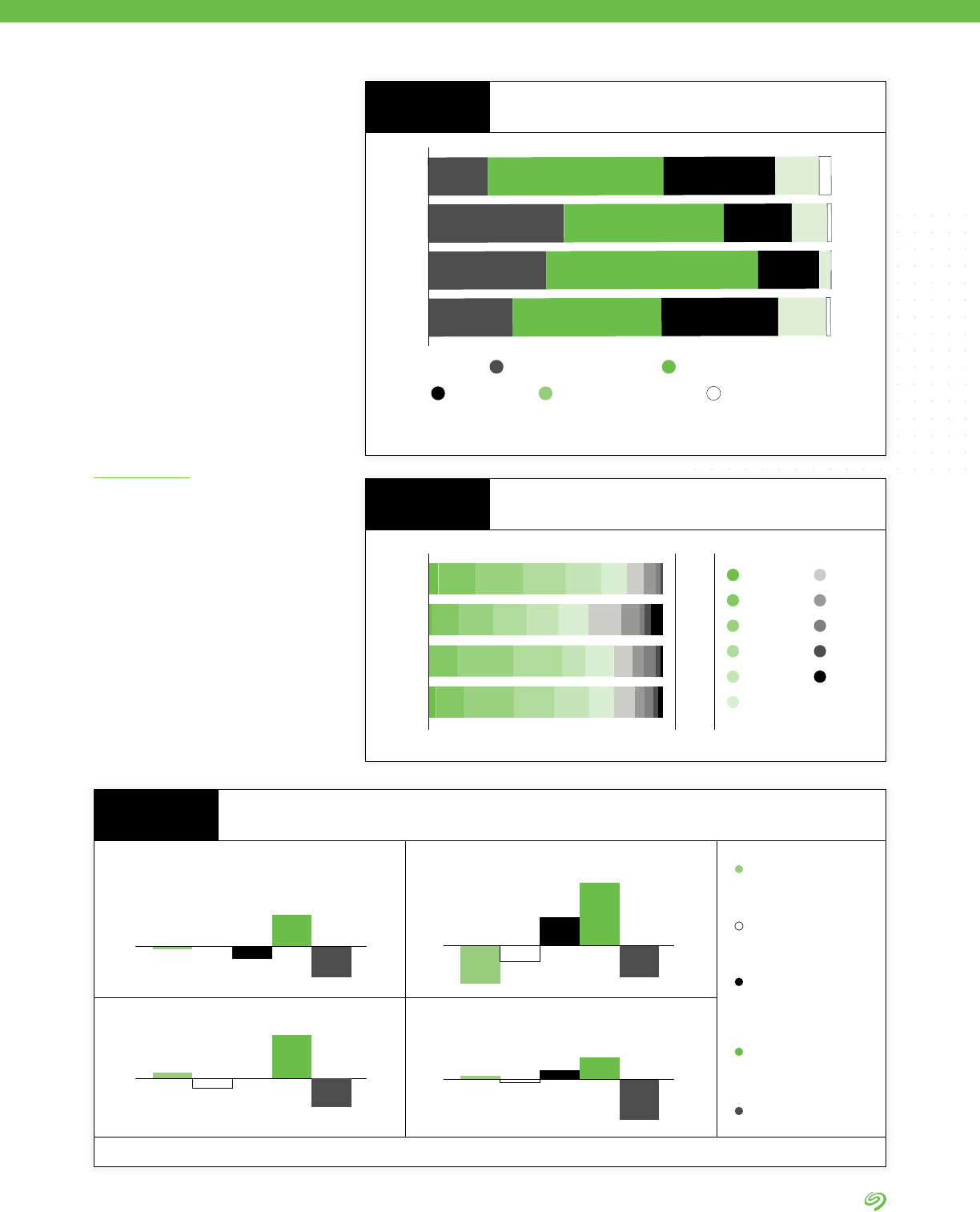

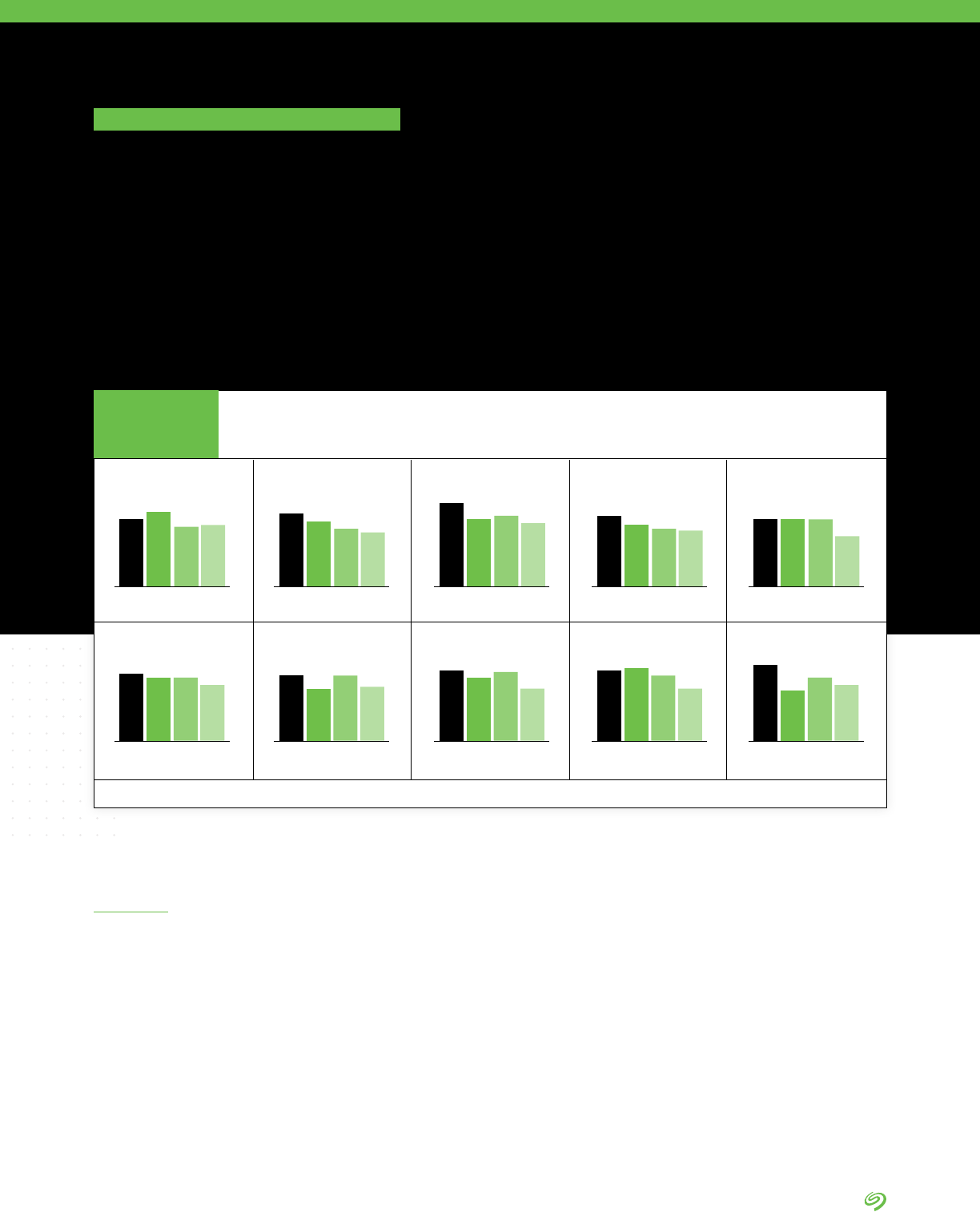

• Managing data in multicloud

environments is the number one

data management challenge

expected in the next two years

by survey respondents.

• Managing data in hybrid clouds

is listed as the second most

important data management

headache.

Takeaways

“Multicloud deployments are much more

difcult to orchestrate and manage

consistently, as the infrastructure tools native

to each cloud platform are typically designed

to operate within the connes of the specic

platform. Furthermore, adjacent services

offered by public cloud providers for data

management or analytics are usually designed

to operate alongside the native public cloud

infrastructure, and may not integrate or be

able to provide full functionality on other

public cloud platforms.”

ANDREW SMITH

RESEARCH MANAGER, IDC

Managing data in multicloud

environments

25% 36% 25% 13%

Managing data in hybrid-cloud

environments

24% 33% 28% 14%

Managing the data connections

between edge and core environments

22% 34% 30% 13%

Deciding what data to keep in what

environments (cloud, on-premise,

edge, etc.)

22% 34% 29% 14%

Getting buy-in to get the resources to

successfully manage data beyond

enterprise data centers

21% 34% 30% 14%

Building or nding the expertise

needed to successfully manage data

beyond enterprise data centers

22% 34% 30% 13%

ChallengingExtremely challenging Somewhat challenging

Not a challenge

Managing Data in More Than One Cloud

Over the Next Two Years

FIGURE 7

DATA BY IDC

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 23 |

According to IDC’s IaaSView

research

1

, the most common use

case for multicloud is to have an

application on one public cloud

IaaS that regularly interacts with

applications on another public

cloud IaaS. This arrangement may

work at the application level.

But at the data management level,

signicant challenges remain:

• separate workows

• disparate management tools

• lack of unied security

management

• the difculty of sharing and

moving large amounts of data

across multiple cloud providers

These challenges add complexity

and time to even the simplest

data-related tasks, like dashboard

creation and reporting in

multicloud environments.

Delving Deeper

Has applications on one public cloud IaaS

that regularly interacts with applications on

another public cloud IaaS

Has applications on one public cloud IaaS

that regularly interacts with applications on

dedicated infrastructure

Has applications that were ported

and/or migrated from one public cloud

IaaS to the other

Has a single set of provisioning,

management, and monitoring tools that

works across all providers

Has similar provisioning and approvals

process across most providers

Is disconnected, with different teams,

provisioning, approvals, management, and

applications for each provider

48%

46%

26%

25%

21%

15%

Level of Integration of Multiple Public Cloud IaaS Providers

FIGURE 8

ANALYSIS BY IDC

Source: IaaSView Survey 2019, IDC

1 IaaSView Survey, IDC, 2019

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 24 |

CHAPTER FOUR

So far, this report has

established that:

• Business data contains a great

deal of value.

• Much of this value goes

untapped, costing business

owners potential revenue.

• An impediment to deriving

optimum value from data lies in

businesses not collecting much

of their data.

But there are other reasons why

data management is a challenge:

issues inherent to the multicloud

ecosystem. This chapter sheds

light on these challenges.

Data Management

Challenges and the

Multicloud Ecosystem

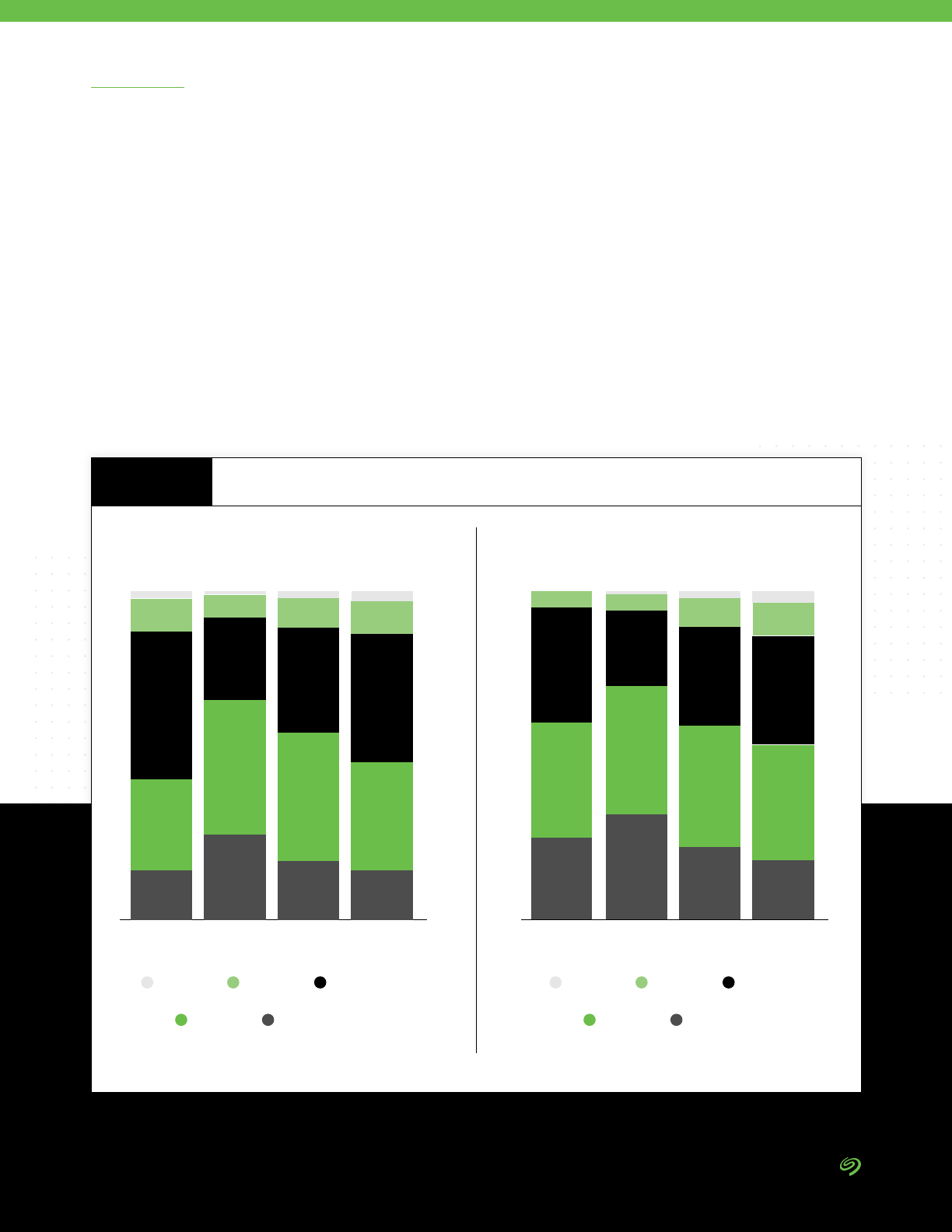

Managing Data

The survey has found that when

it comes to managing one of their

most valuable resources—data—

enterprises report being unable to

successfully control the growing

complexities on their own. They

report that they need help with data

management.

A key reason for this is a wide and

relatively even distribution of data

across edge and cloud repositories.

There is some variation: the

transportation and electric vehicles

industry shows most data at the

edge, while the manufacturing

sector stores more data in internally

managed data centers.

DATA BY IDC

Internally managed

enterprise data centers

Third-party managed

enterprise data centers

2020

30%

Other locations

9%

20%

Cloud repositories

(public, private, industry)

22%

Edge data centers

or remote locations where

data is stored

19%

Where Data Is Stored Currently

FIGURE 9

SEAGATE POV

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 25 |

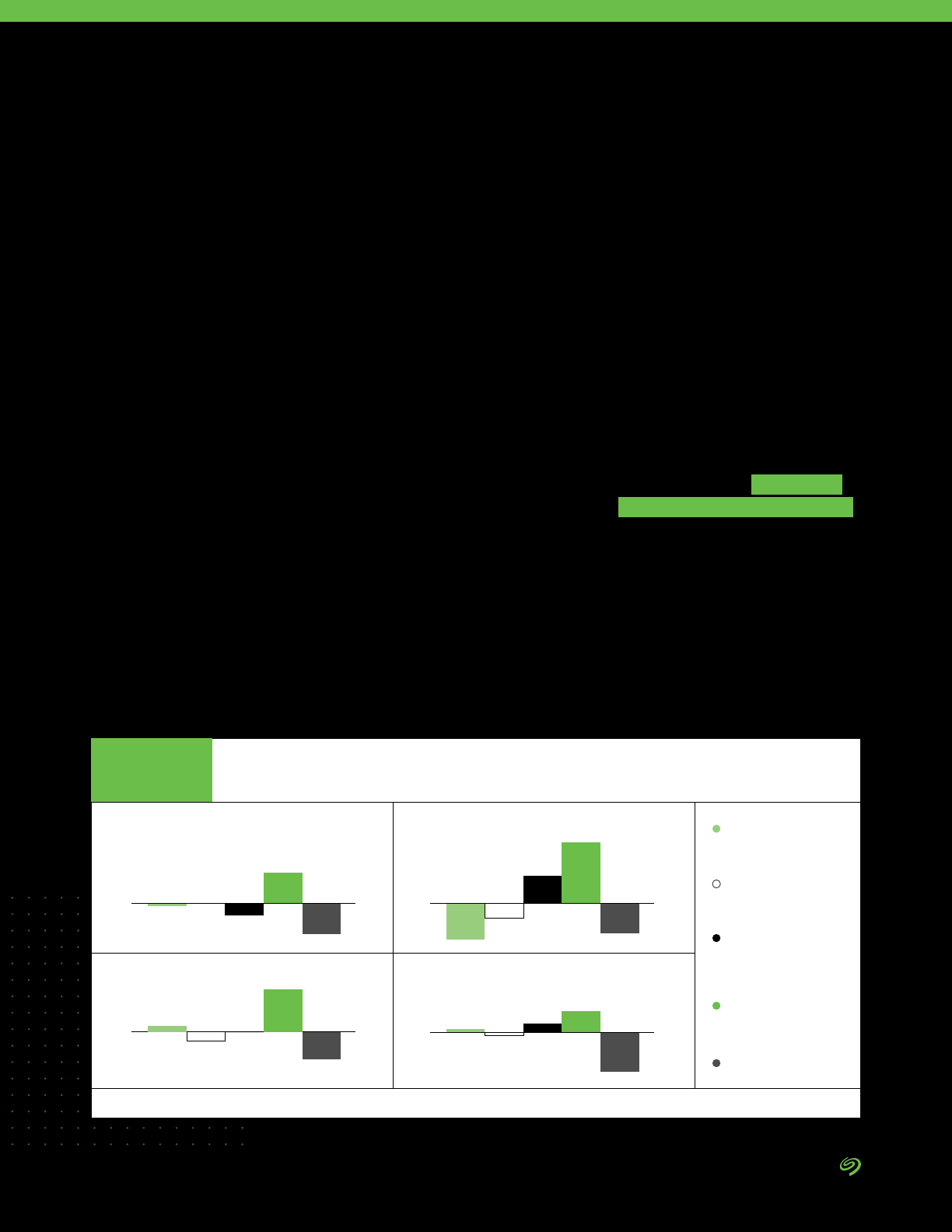

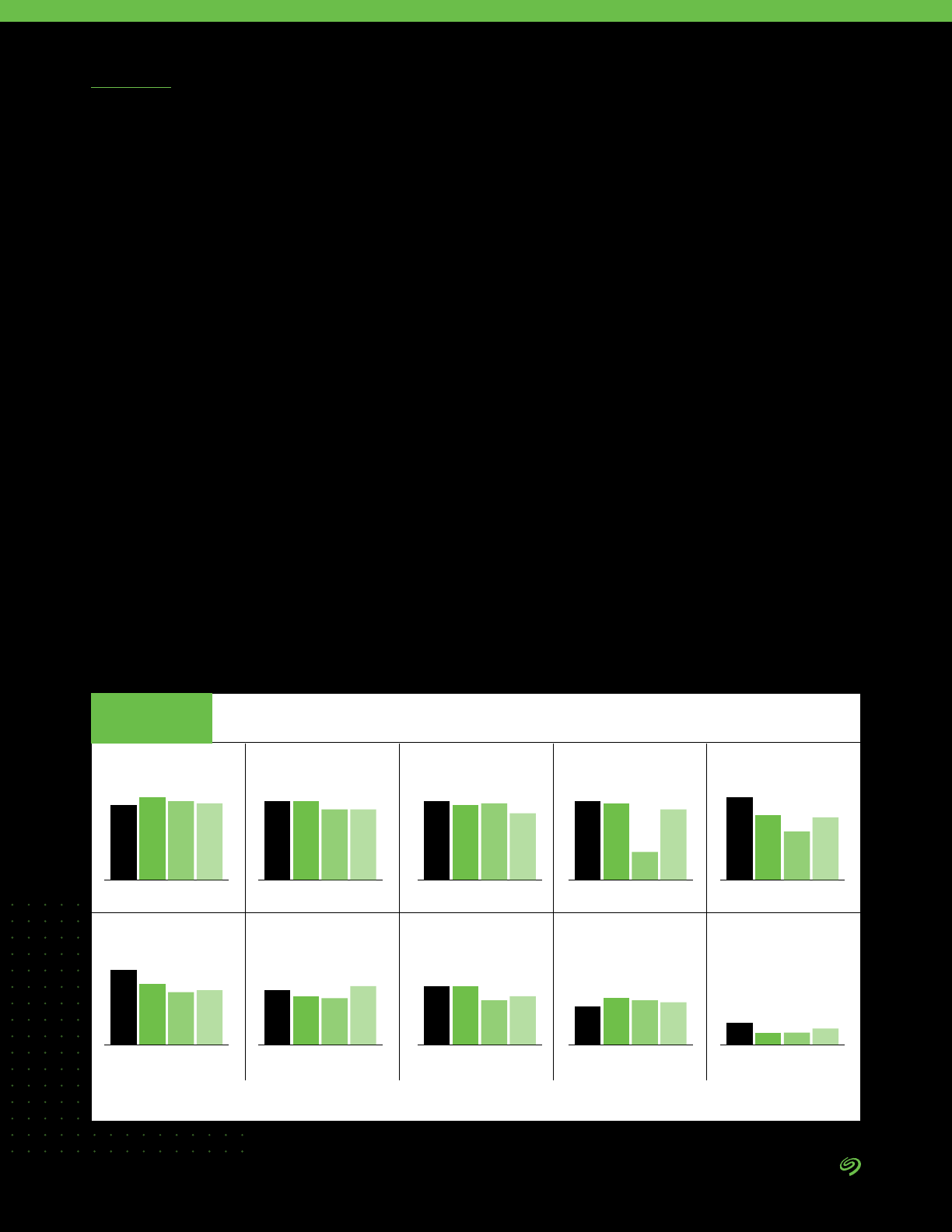

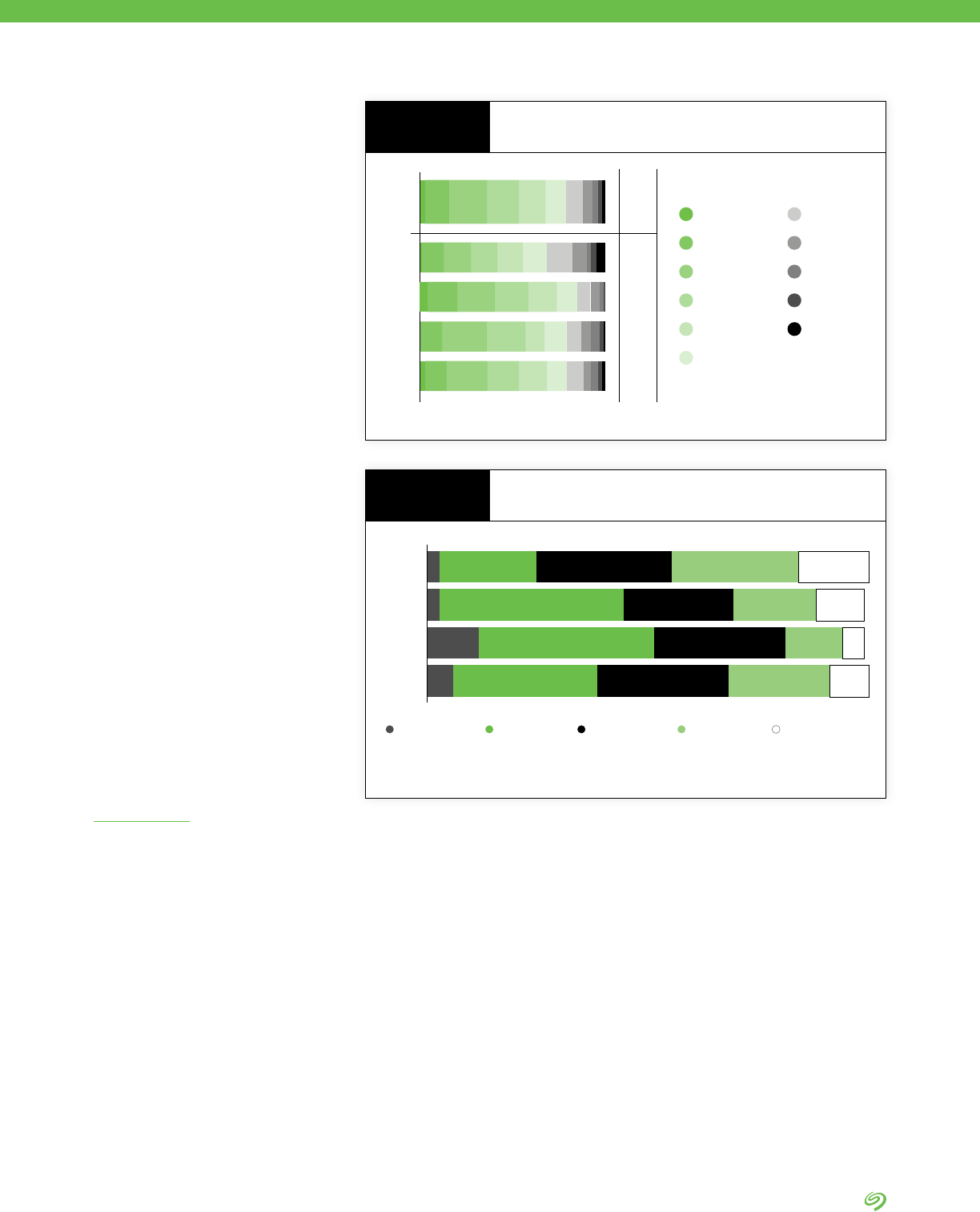

When asked what was the most

important factor driving the changes

being made to the organization’s

approach to how it manages central

storage needs:

• 17% of respondents pointed to

improving data security

• 14% quoted increasing access

for data analytic and management

services (AI/ML, IoT, etc.)

• 14% noted increasing visibility

and manageability of IT

infrastructure operations

• 11% listed reducing cost/TCO of

infrastructure

• 10% mentioned providing faster

access to data for applications

and business units

Third-party managed

enterprise data centers

Internally managed

enterprise data centers

2020

2022

Edge data centers

or remote locations where data is stored

Cloud repositories

(public, private, industry)

Other locations

2022

2020

2022

2020

2022

2020

2022

2020

2022

2020

9%

8%

22%

25%

19%

19%

30%

28%

20%

20%

Where Data Is Stored Now vs. Two Years From Now

FIGURE 10

Driving Changes in

Data Management

Improving data security

17%

14%

14%

11%

10%

9%

9%

8%

8%

Increasing access for data analytic and

management services (AI/ML, IoT, etc.)

Increasing visibility and manageability of

IT infrastructure operations

Reducing cost/TCO of infrastructure

Providing faster access to data for

applications and business units

Meeting increases in data

capacity requirements

Improving ease of use

Improving availability and

increasing uptime

Integrating third-party services to use

alongside modern infrastructure

Driving Factors in How Data Is Stored

FIGURE 11

Source: The Seagate Rethink Data Survey, IDC, 2020

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 26 |

Before business owners

implement the steps to better

manage data, they need to

understand their own data.

Unfortunately, most organizations

have a tendency to collect and

dump data into large repositories.

But when they merely collect

tons of data, they will struggle

to make sense of it. If they don’t

understand their company’s data,

then they don’t know what data

they need to collect and what

intelligence they can get out of it.

Business leaders’ rst task is to

dene why they want to collect data

and what insights they are trying to

gain. Only once they are clear on

that agenda should they go after

that particular goal—as opposed to

the kitchen sink approach.

Collecting data is easy.

Intelligence is hard.

To smartly collect and sort through

data, enterprises need to deal with

challenges of overlapping tools, data

complexity, data integration, ensuring

that data is “clean,” ensuring proper

data correlation, etc.

Collecting data has to be about

what enables the business objective

(what business owners want to

learn). Unless they gure this out,

amassing data won’t provide them

with the value they expect.

Take, for example, manufacturing.

Many industries adopted large

volumes of IoT devices and

platforms, endpoint devices with

sensors, as well as ML and AI

to manage their manufacturing

ecosystems. Data collection

happens at unprecedented

volumes. Business owners can

collect a great deal of data. But

without understanding what they

want out of their data, it can be

difcult to accomplish basic goals—

for example, to improve throughput

of manufacturings—if the factories

are ooded with tens of thousands

of uncoordinated IoT devices

deployed on different platforms.

Business Owners, Stop (Merely) Hoarding Data

Another way to achieve successful

data management is through

smart data storage solutions.

Challenges arise as a result of a

conuence of factors:

• Nonstandard architectures

• The proliferation and

coexistence of different storage

technologies

• Difculties managing the storage

technology footprint

• Lack of visibility, or the so-called

single pane of glass, of stored

data’s management (object and

le storage show up differently)

• Deciding which data goes where

• Prohibitive costs play a role in

decision-making about storage

solutions

• Inability to look at a multicloud

storage pool as a whole

between on-prem and cloud

A key solution to these data

storage management challenges

has to do with how business

owners see the stored data. The

idea is to see it—all of it—as if

through a single pane of glass. It

goes beyond data democratization

and into storage unication. CIOs

should be able to look across the

multiple cloud ecosystems in a

seamless manner.

Data Storage, Through a Single Pane of Glass

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 27 |

This challenge, meaningfully

shown by the shift of data to the

multicloud ecosystem, can be

solved by storing data in clouds

that allow enterprises control

over their data (on premises,

private clouds, or the rare public

clouds that do not come with

data lock-in).

Another solution on the horizon

is storage virtualization, which a

number of companies are working

to innovate. In this scenario,

the single pane of glass would

be a data storage management

software layer.

Bottom line for business owners:

ownership of your data starts with

an unobstructed, easy view into it—

as if through a single pane of glass.

Data Management

Challenges

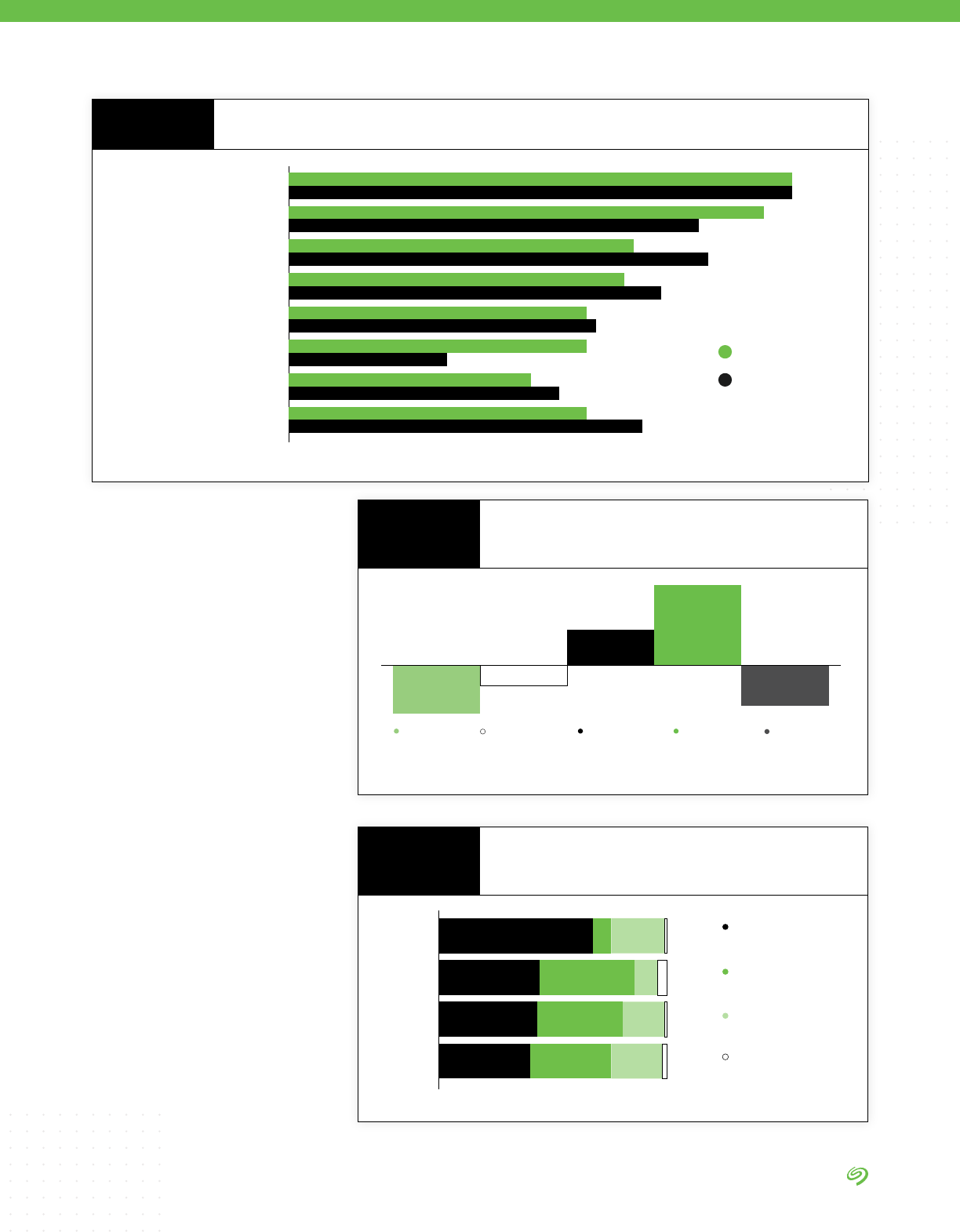

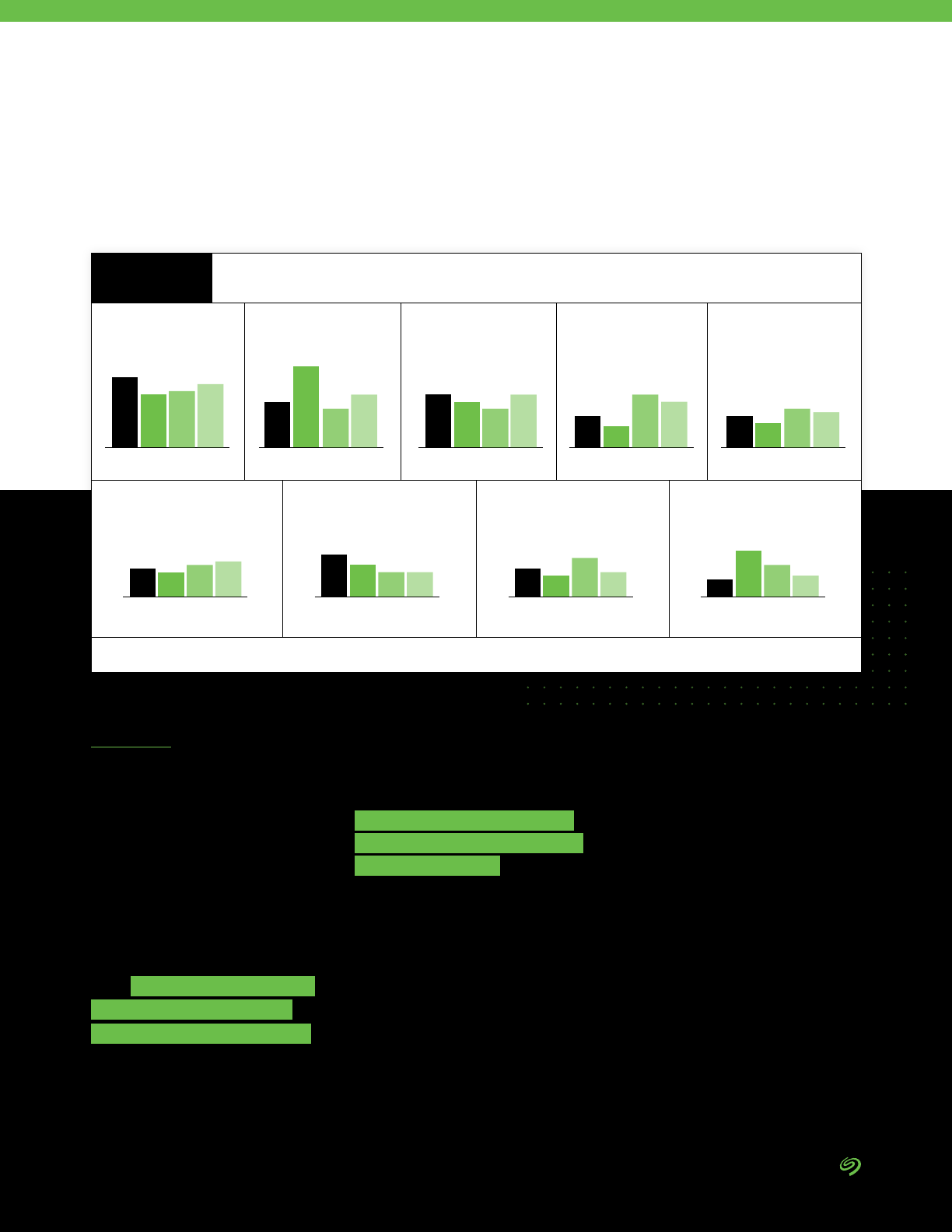

Organizations face ve key

challenges that they believe limit

their ability to exploit the full

potential of collected data:

1. Making collected data usable

2. Managing the storage of

collected data

3. Ensuring that needed data is

collected

4. Ensuring the security of

collected data

5. Making the different silos of

collected data available

DATA BY IDC

These considerations are put

in the language of IT. But they

should matter to business owners

because they directly affect the

value of data that businesses can

uncover, which affects revenue (as

we’ll see in chapter 6.) Modern

data management solutions

should focus on resolving these

challenges to provide the most

effective experience possible

for both business owners and

customers, and begin to help

businesses chip away at the

percentage of data that they are

unable to exploit.

In the following chapter we learn

about the one reported missing

link of data management that can

help make this happen.

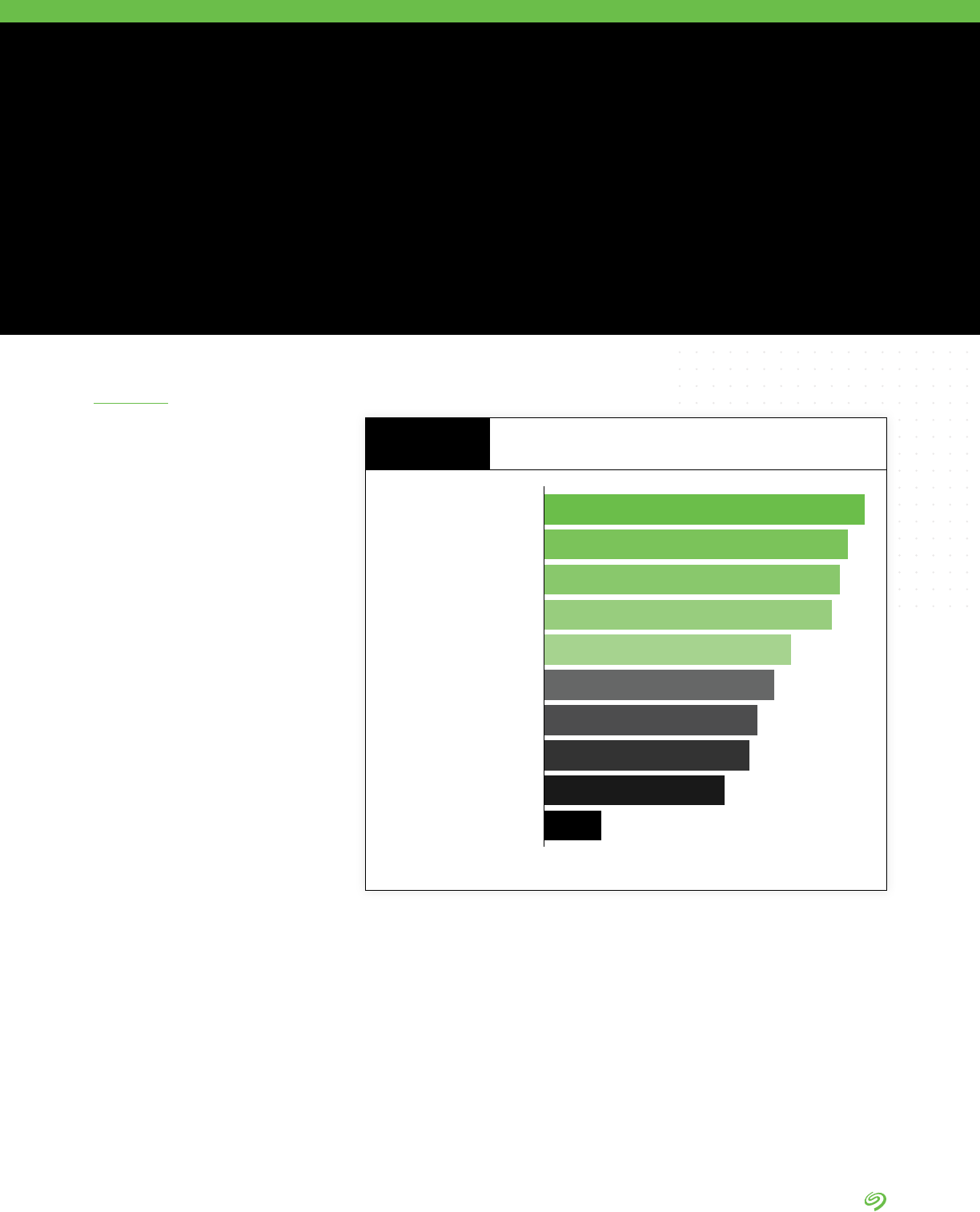

Making collected data usable

39%

37%

36%

35%

30%

28%

26%

25%

22%

7%

Managing the storage

of collected data

Ensuring that needed

data is collected

Ensuring the security

of collected data

Making the different silos of

collected data available

Getting the required resources

to manage collected data

Having the technology in

place to analyze data

Establishing data management

governance and processes

Building the people resources

needed to analyze data

Connecting the curated

data with data users

Barriers to Putting Data to Work

FIGURE 12

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 28 |

In our survey data, the

manufacturing industry has

distinguished itself as a data

management laggard of sorts.

Perhaps counterintuitively, the

sector shows the lowest level

of task automation in data

management, and lowest rate for

full integration (single platform) of

data management functions.

• Manufacturing lags in both

multicloud and hybrid cloud

adoptions.

• Along with the telco and CDN/

media industries, it indicates

below-average satisfaction with

its data management approach.

• Along with telco, respondents

in manufacturing indicate

low satisfaction with data

management tools.

• Manufacturing’s greatest data

management challenge is storage

management.

Additionally, manufacturing

indicated one of the lowest rates

of data growth of any industry

(37% vs 42.2% on average).

However, the sector has the highest

enterprise data center footprint (on

premises) of any surveyed industry.

This may provide insight into why

manufacturing has a lower rate of

data growth: they are slowed down

by on-premises infrastructure that

is likely more difcult to expand

in terms of capacity (especially

when compared to scalable cloud

infrastructure).

An argument can also be made

that while manufacturing generates

a signicant amount of sensor and

device-related data, much of it is

produced at the edge and discarded,

rather than transferred to a core

environment for long-term storage.

Manufacturing also indicated the

lowest levels of automation of data

management functions—and the

lowest rate for full integration of data

management functions on a single

platform (just 9%, compared to 19%+

in all other industries). Both of these

data points may be driven by the

sheer number of connected assets

entering modern manufacturers.

As IDC’s Manufacturing Insights

2018 IT and OT Integration

Survey showed, nearly 80% of

instrumented production assets

are digitally connected in some

form. The question is why does

this disconnect between digital

assets and data management

exist within the manufacturing

industry? IDC research has identied

two important challenges to consider

alongside this survey analysis:

1. Manufacturing faces a major skills

gap. If skilled people represent

the ultimate opportunity for the

factory of the future in developed

economies, the lack of adequate

skills is one of the toughest

barriers that companies need to

address. They are dealing with

aging workforces and challenges in

nding new skilled employees willing

to work on the plant oor when it

comes to hard and soft IT skills.

2. Most manufacturing plants are

lucky if they can connect to half

of their assets on the oor. This

isn’t just about applications, data

centers, and networks; it’s also

about core enterprise architecture

and infrastructure decisions

such as IT/OT integration and

security. In many cases, legacy

infrastructure simply won’t be

able to keep up with the amount

of connected assets entering the

plant. As a result, many plants

may implement ad hoc processes

to connect and manage assets

without being able to rely on

underlying infrastructure for

comprehensive management.

Manufacturing: An Outlier

ANALYSIS BY IDC

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 29 |

CHAPTER FIVE

In the age when the volume of data

is proliferating at unprecedented

speed, how do enterprises

manage all this data in a way that

taps its value and satises both

shareholders and customers?

The survey identied a key solution

to this data management quandary:

DataOps. Throughout the global

business landscape, DataOps

looms as the missing link of data

management—and the solution to

business owners’ data headaches.

DataOps, dened by IDC as the

discipline connecting data

creators with data consumers,

should be part of every successful

data management strategy.

DataOps is part of data

management. In addition to

DataOps, data management

includes data orchestration

from endpoints to core, data

architecture, and data security.

The goal of data management is

to facilitate a holistic view of data

and enable users to access and

derive optimal value from it—both

data in motion and at rest.

Given what we’ve learned in the preceding

sections, a conundrum emerges.

DataOps: The Missing Link

of Data Management

DataOps

Across regions and industries,

only an average of 10% of

organizations report having

implemented DataOps fully across

the organization. The opportunity

is there for the taking.

DataOps is neither a technology

nor a process, but rather an

emerging discipline of connecting

data consumers with data creators

to enable collaboration and

accelerate innovation.

DataOps capacity

has been fully implemented

across the organization

DataOps capacity

has been partially

implemented

Have started to build

DataOps capacity

Considered and

planning to build

DataOps capacity

Not considered this

separately at all

Tota l

33% 30%7% 21% 10%

Transportation/EV 39% 28%7% 17% 9%

Telecommunications

31% 35%8% 17% 9%

Media

28% 32%9% 18% 12%

Manufacturing

39% 32%5% 19% 5%

Other

32% 27%6% 25% 10%

The State of DataOps

FIGURE 13

DATA BY IDC

SEAGATE POV

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 30 |

Data consumers are people

within business units who

are responsible for driving

the organizational decision-

making—whether toward product

development, product distribution

and marketing, cost control,

operations, etc. Common data

consumers are general managers,

VPs, CXOs, and the people who

support them. Data consumers

really don’t need data; instead,

they need actionable information.

Data creators can be both

machines—such as endpoint

and IoT devices—and people

who generate the reports and

information that is fed to decision-

makers. The challenge for data

creators is often to determine

what data must be collected for

prompt activation and what should

be collected for retention. For

example, the health of a device

(e.g., whether it’s running) may

not necessarily require immediate

processing and can be moved to

long-term archiving. However, data

about the device’s operations (e.g.,

temperature, capacity, speed, etc.)

may need immediate analysis or

coordination. This sort of data can

lead to better predictive analytics,

event correlations, and so on.

DataOps can exploit technology,

in particular AI and ML, to assist

in correlating data from core,

cloud, and edge data sources.

DataOps also utilizes ELT-like data

ingest functionality (Extract. Load.

Transform.) to pull data from multiple

sources and load into a common

structure, frequently as a data lake.

AI can be a key for transforming

data into the information needed by

decision makers.

Being able to correlate data from

disparate sources is a capability

not easily available through other

means. Because it is difcult,

those organizations able to master

it can expect to have an edge over

the competition.

The survey revealed that most

organizations have multiple tools

to perform a similar function,

which makes enterprise data

management a challenge.

In fact, only about one third of

organizations reported having

a single solution for a single

function. This may be caused

by a variety of reasons: different

buyers within the organization,

incompatibility of solutions across

platforms, or simply historical

evolution of the systems.

Back up/Recover

Container orchestration

Policy management

Data discover

Data classication

Metadata management

Recovery orchestration

Data security for data being stored

Data security for data on the move

Data migration, tiering, or placement

34% 47% 16% 3%

33% 41% 20% 6%

38% 41% 18% 3%

33% 46% 19% 3%

33% 47% 17% 3%

33% 44% 19% 4%

32% 45% 18% 5%

34% 45% 18% 3%

34% 45% 18% 3%

34% 46% 17% 3%

Not sure

Apps deployed in

some locations

or for some

applications

Multiple apps

deployed enterprise-

wide in all locations

Single app deployed

enterprise-wide

in all locations

Approach Used to Deploy Tools or Applications for

Data Management Functions

FIGURE 14

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 31 |

While it may be necessary to have

point products at a system level,

it is essential to have a unied

data management capability.

DataOps is the practice of bringing

disparate data systems into an

understandable entity. The core

functionality needed for DataOps

is metadata management,

data classication and policy

management. As data is ingested,

the metadata management function

allows data to be associated

and managed based on its

characteristics. This metadata,

along with data classication

capabilities, can identify specic

types of data, such as personally

identiable information (PII) and data

governed by the Health Insurance

and Portability and Accountability

Act (HIPAA). Once data is classied,

AI algorithms can be developed to

automatically recognize data and

make associations.

DataOps is particularly well suited

to the iterative learning approach

required by AI-driven applications.

This approach is the reverse

of the traditional data analytics

approach. Traditional analytics

takes a problem and searches

for an answer; DataOps makes

data associations and searches

for insights. For example, data

may reveal that consumers make

seemingly unrelated product

purchases together, leading to

better merchandizing or product

placement; or it may spot trends

within certain demographic groups

leading to focused micromarketing.

It is not always technology only

that stands in the way of effective

DataOps. Business owners need

to be aware of culture and people

challenges.

When organizations operate

in silos, too often different

competing groups work toward

their own objectives. They want

to gain and keep control of data.

The mindset is, if they lose control

of the data, they lose power,

because data is power.

As a result, data is stored,

managed, and analyzed in silos.

If various groups within an

organization access the same raw

company data and each group

does analysis, their reports do

not often match because they

don’t avail themselves of a global

repository of data.

The solution to this people problem

needs to start with the business

owner’s strategy. That strategy

needs to institute global standards,

global data architecture, global

data management, and the same

access to the same analytical tools

by global teams.

Rolling back reporting functions

to IT can provide global tools,

capabilities, and solutions

that every group can leverage.

The various groups within the

enterprise should get out of siloed

management of their own data,

and allow the IT-instituted tools to

do that globally.

In doing so, the teams will be

freed to make decisions based

on insights from reliable, global,

accessible pools of data.

DataOps: The Human Element

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 32 |

• Majority of respondents say

that DataOps is “very” or

“extremely” important

• DataOps is seen as most

important in North America and

China (see Section II for the

regional analysis)

• While DataOps is considered

important across all industries,

transportation shows a slightly

higher need for it than other

industries

• While this survey was done

prior to the COVID-19

pandemic, DataOps is going

to be even more needed as

more people continue to rely on

working from home, which has

already accelerated migration to

cloud services.

Business leaders all over the globe agree with the need for DataOps.

Not very

important

Somewhat

important

ImportantVery

important

Extremely

important

Total

NA

China

Europe

APJ

42% 24%23% 10% 1%

40% 17%34% 9% 1%

0%

52% 15%29%

44% 28%15% 11% 3%

37% 29%21% 12% 1%

3%

Importance of DataOps

FIGURE 15

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 33 |

CHAPTER SIX

The ndings make clear that in

large part the solution to data

management puzzles can be

found in implementing DataOps—

the discipline that connects data

consumers with data creators,

and the processes that go with

it. How do we know DataOps is

useful? The survey results point

to a signicant result.

Along with other data

management solutions—

analytics-enabled data

orchestration and well-functioning

data architecture—DataOps

leads to measurably better

business outcomes. Among them:

improved customer loyalty and

satisfaction, better prots, higher

revenues, and greater employee

retention and productivity.

DataOps therefore has a

demonstrated bearing on an

enterprise’s competitive edge.

At last, we come to the truly good news that the

survey delivers to business owners.

Better Business Outcomes

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 34 |

A Competitive Edge

Efcient DataOps is the foundation

for rapidly building and training AI

models and for deploying analytics

at scale. These advanced

analytical results can lead to

competitive advantage.

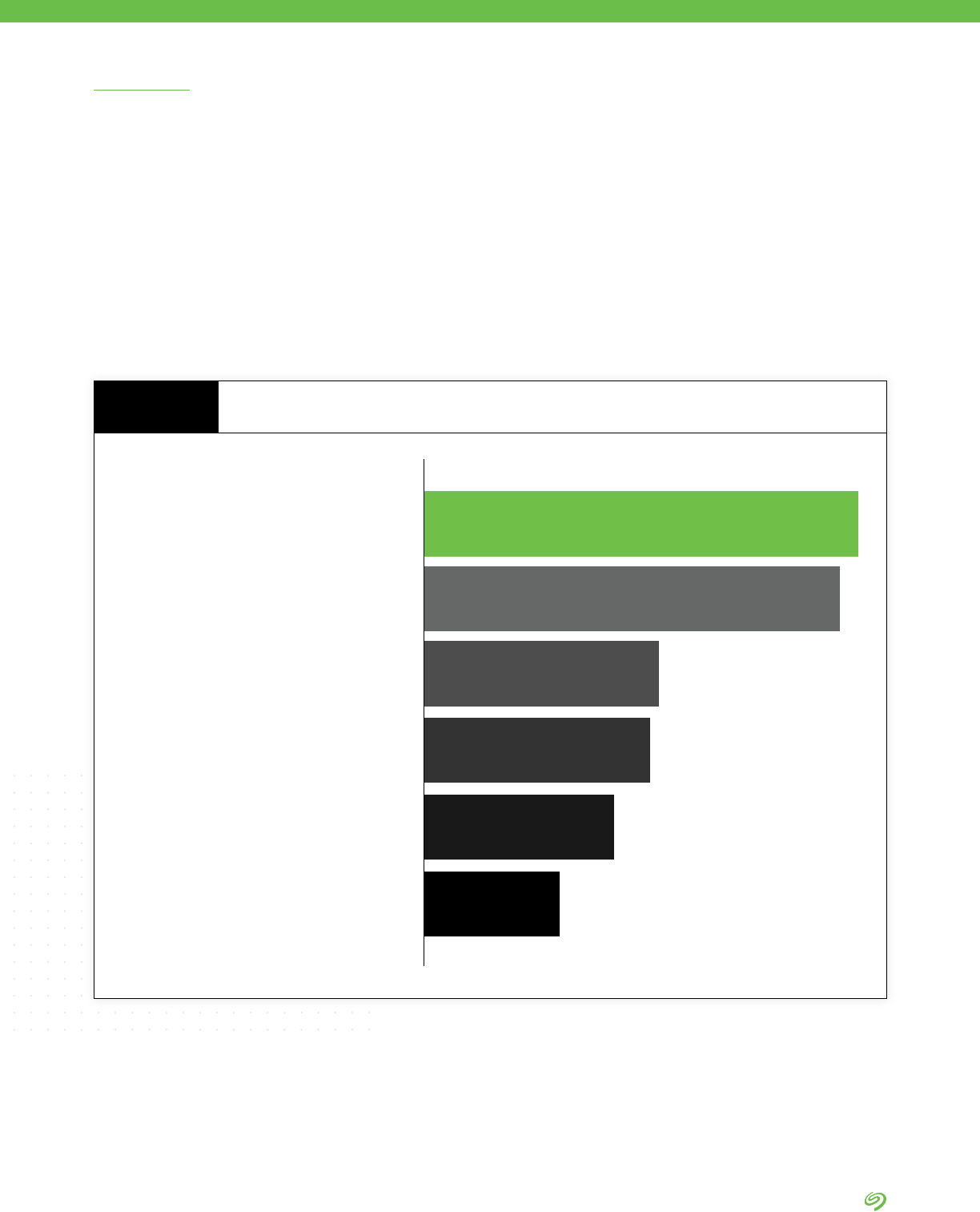

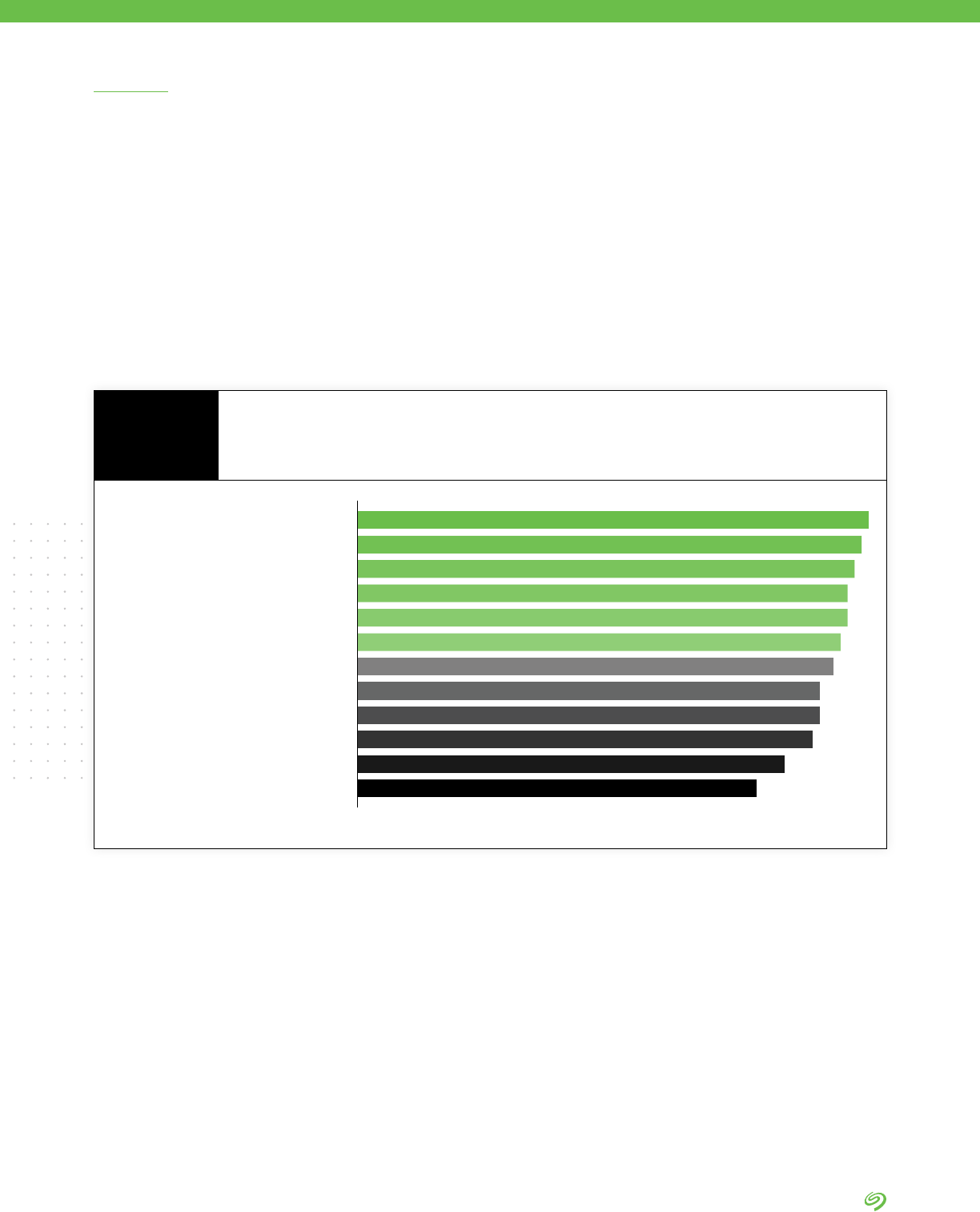

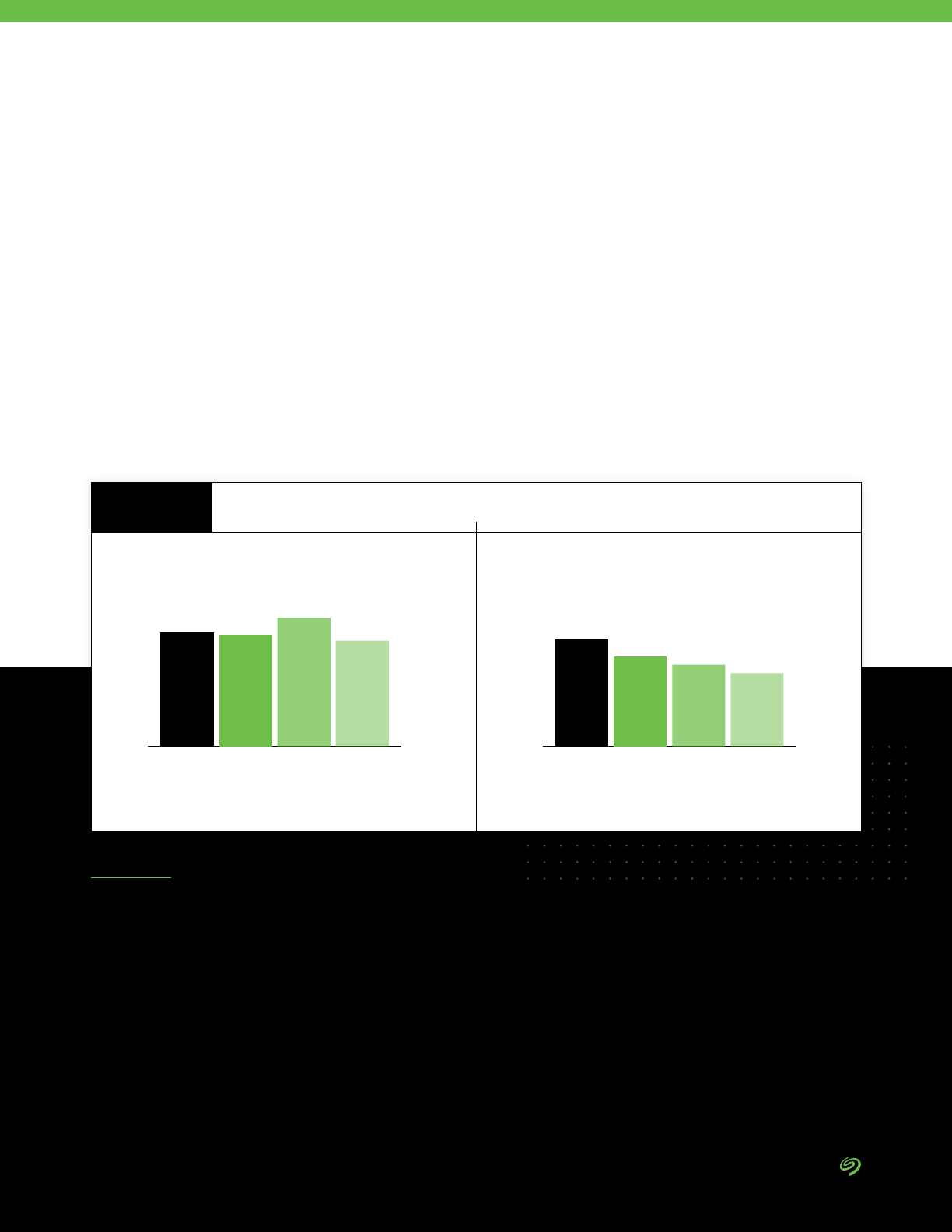

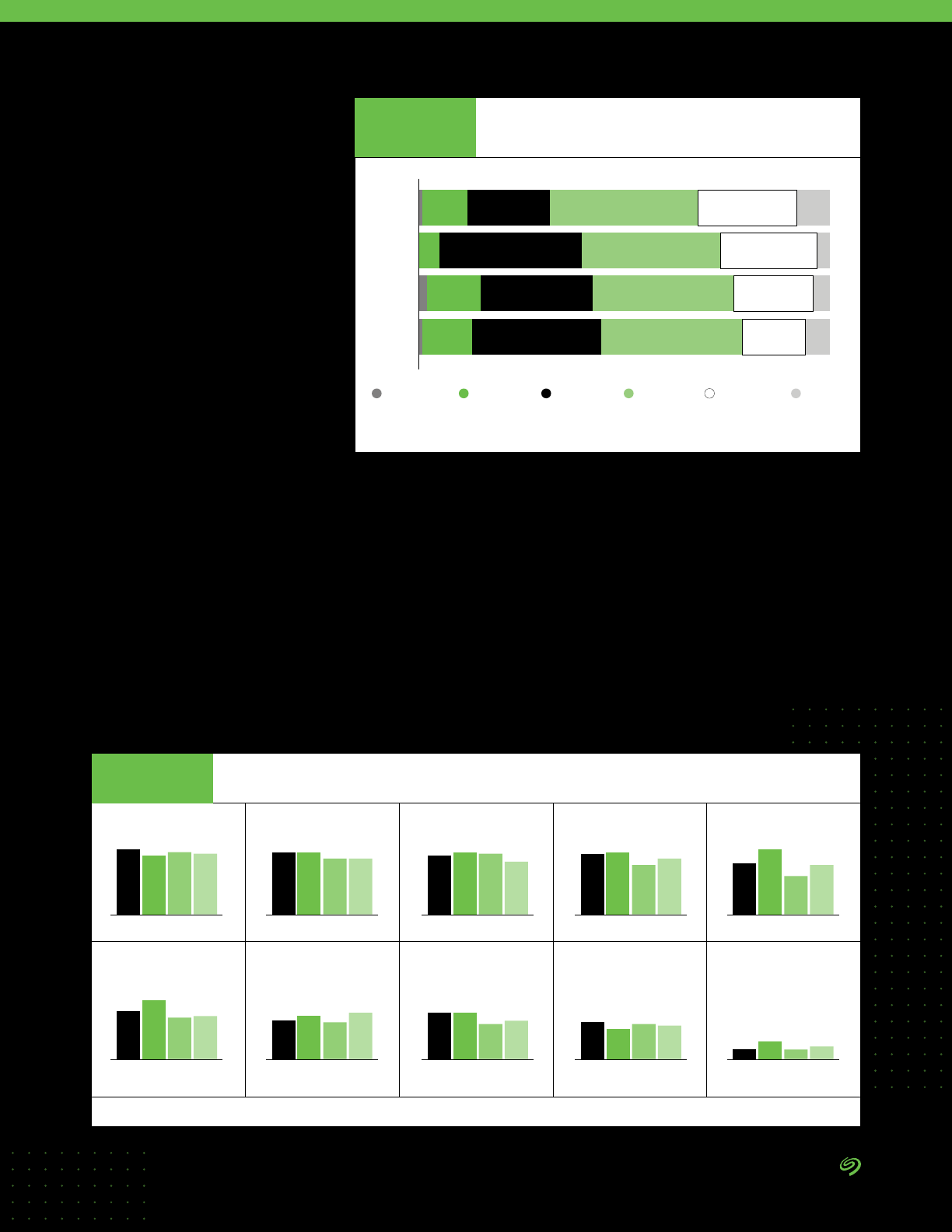

The survey found that better data

analysis leads to measurably better

business outcomes.

The following chart points out

the areas of improvement from

organizations that cited having

improved data analytics. Note that

speed of improvement makes a

difference, since most organizations

can say they improved over time.

The companies that improve fastest

can expect better business results

compared to peers. Though the

results in Figure 16 do not reect the

effect of DataOps alone, DataOps is

the latest and leading-edge method

for improving data management.

For most organizations, the trifecta

of better business outcomes is the

following:

1. Better revenue.

2. Better prot.

3. Better customer satisfaction/loyalty.

But better results due to data

management and analytics were

seen across the enterprise and

also included:

• Better employee productivity.

• Better employee retention.

• Lower costs.

• Improved regulatory compliance.

• Better new customer acquisition.

Among the more proactive

results is better new customer

acquisition, which obviously is the

key to growing revenue.

DATA BY IDC

Employee productivity

Revenue

Prot

Customer satisfaction/loyalty

Customer retention

Employee retention

Adherence to regulatory compliance requirement

Operational costs

Shorter time to market for new products and services

New customer acquisition

Number of new products and services offerings

Reduction in CapEx requirements

73%

72%

71%

70%

70%

69%

68%

66%

66%

65%

61%

57%

Indicators Used to Measure the Success of Investments in

Data Management and Analytics in Improving Performance

of the Organization

FIGURE 16

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 35 |

DataOps: Getting to Customer Satisfaction and Prot Through Data

This survey established that a

smooth-functioning DataOps is key

to data management that enables

organizations to get more value

out of data and boosts business

outcomes such as prot and

customer satisfaction.

How can businesses get there?

As noted in the preceding section,

the human element of the equation

cannot be overstated. It’s the

people who keep data in silos.

Consequently, the way to institute

effective DataOps is not just about

having the right tools. To be sure,

the right tools are key. Virtualization

tools are immensely useful, if not

necessary, in that they allow for the

retrieval and manipulation of data.

Whether it’s a software virtualization

plane (such as Kubernetes, “a

portable, extensible, open-source

platform for managing containerized

workloads and services, that

facilitates both declarative

conguration and automation”)

or virtual machines that are an

abstraction mechanism for app

deployment, virtualization layers can

streamline data management.

But before DataOps avails itself

of virtualization, it has to start with

decisions about data. Putting tools to

work is the easy part. It’s trickier for

enterprise leaders to make decisions

about data via data governance and

processes around it.

Business owners need to start

with their goals—which commonly

include boosting customer

satisfaction and prot. To get

there, they need to interrogate

the data at their disposal.

They need to coordinate data

from various sources and solve

governance issues such as:

• Who has access to what data?

• How to classify data?

• Which data to keep and where?

• What to do with data after it’s

analyzed?

• How to make data available?

• How to interconnect data?

In order to make these

determinations, business owners,

data administrators, or CIOs

need to consult subject matter

experts (SMEs). Along with

SMEs, they need to identify,

evaluate, cleanse (detect and

correct inaccurate records),

and validate data. SMEs need

to be at the table because only

they possess deep knowledge of

certain types of data.

It’s with the involvement of the

SMEs, under the direction of

business owners, and facilitated

by data administrators that

determinations need to be made

regarding a key question: What

intelligence do you want out of

what data? What do you want it to

tell you? How do you want to use it?

There can be about 10,000 entry

point parameters collected for a

single product that a company

manufactures. If the company is to

retain all these points of information

for just one product, without a

clear data architecture dening

where it will all be stored and how

it will ow between environments,

the data risks drowning in a data

swamp. The decision-makers

need to confer with product design

engineers and quality engineers,

and ask: Which of the 10,000

parameters are the most critical?

Then, through interrogating and

tracking the curated data, they are

on a more efcient path to building

components and solutions.

The upfront work of data

governance—involving

coordination, discussion, analysis,

agreements around language,

and data classication (more on

this in the following chapter)—can

give way to the mostly-automated

downstream processes facilitated

by virtualization tools.

This twofold process of DataOps

can then reap the results of

customer satisfaction because

optimizing the governance and

ow of data leads to better quality

of offerings, which directly affects

how customers feel about their

purchases. As IDC analysts pointed

out in the previous chapter, speed

of delivery matters too. Getting

to results faster means greater

customer satisfaction—because

getting to data faster means

customers and business owners

can make decisions faster.

This is how a process that starts

with business owners setting out

to increase customer satisfaction

and prot attains these very goals

through optimizing data via DataOps.

It’s about being intentional on

making the most of data.

SEAGATE POV

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 36 |

CHAPTER SEVEN

In addition to DataOps, a unique part of data

management that deserves a special examination

is data security.

Data Security and Data

Management

Two thirds of survey respondents

report insufcient data security,

making data security an essential

element of any discussion of

efcient data management.

Data security is consistently rated

among the highest concerns and

priorities of IT leaders and business

leaders alike. Data breaches lead

to direct nancial losses, signicant

regulatory nes, reputational

loss and embarrassment, lost

customers, and more. Malware

attacks can result in the theft of

corporate secrets, lost employee

productivity, unrecoverable data,

and, in the case of ransomware,

nancial loss and embarrassment.

However, many organizations

surveyed have not implemented

common data security practices

enterprise-wide (Figure 17).

The results in Figure 17 do

not represent an all-or-nothing

approach to enterprise security.

That is, a respondent might answer

“yes” to encryption of data at rest,

but “no” to all others, for example.

Thus, it is highly probable that

the vast majority of organizations

have at least some signicant

vulnerabilities in their environments.

DATA BY IDC

Encryption of data in ight

Physical security of

data storage facilities

Employee training for handling

sensitive information

Encryption of data at rest

Masking of data

Location and movement

restrictions on data

36%

34%

34%

32%

32%

32%

Percentage of Organizations Fully

Implementing Key Security Practices

FIGURE 17

Source: The Seagate Rethink Data Survey, IDC, 2020

RETHINK DATA: PUT MORE OF YOUR BUSINESS DATA TO WORK—FROM EDGE TO CLOUD | 37 |

The biggest myth about enterprise

data security is that the technology

is the hard part; it’s not.

The challenge is getting alignment

on classication of data by risk

and on how data should be stored

and protected. That, as in the case

of DataOps, is the human element.

Technology boils down to

business owners’ purchasing

decisions. You want to protect

data at rest? Buy self-encrypting

drives; problem solved.

Educating data users—those

within the company who

create, touch, analyze, and

move the data—is a different

matter. Business leaders should

remember that the more data

creators and consumers within

their company are educated, the

better for the business. Business

owners’ own education about

data security is key to success,

because it ensures their buy-in.

The education about data security

should be democratic. Protecting

data (and the education that